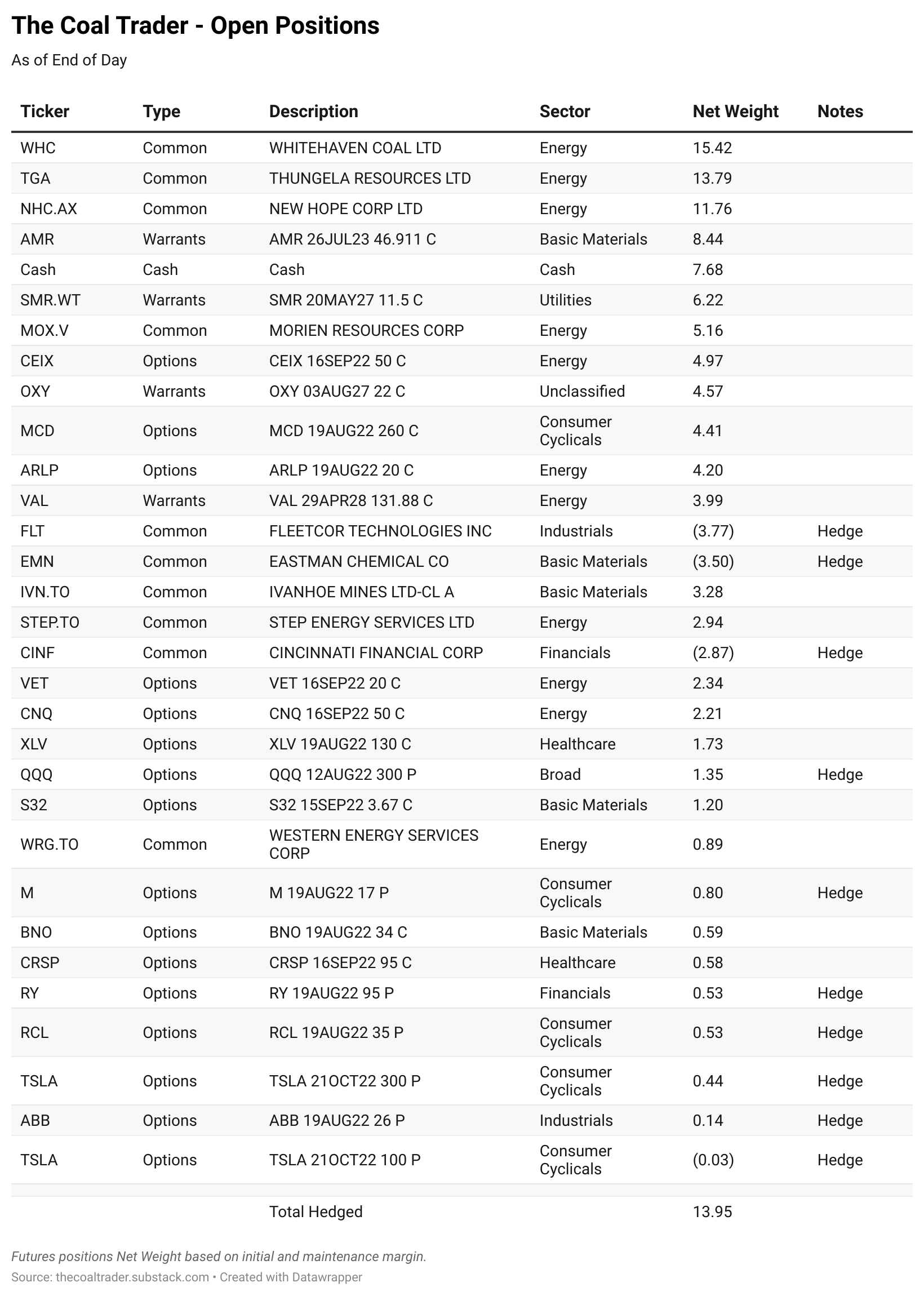

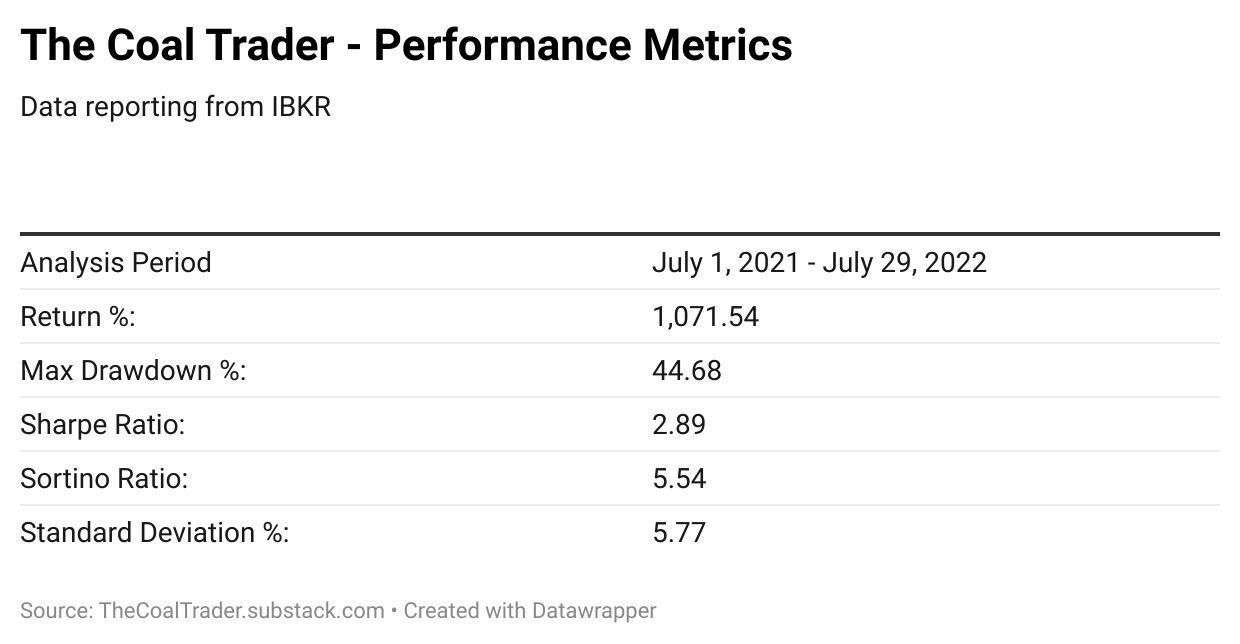

Portfolio Weightings & Performance

Daily Commentary & Positioning - Week of July 25, 2022

The following is daily commentary for the Week of July 25, 2022. You can scroll down to see portfolio positioning throughout the week along with various performance metrics. This post gets updated every morning prior to market opening so be sure to check back for daily updates.

Monday 7/25/2022

Thermal coal markets continue their upward trajectory, and coal equities are finally playing catch up as we approach earnings for US names in the coming weeks. WHC.ax, CEIX, and ARLP remain the horses to ride as positive coal fundamentals are quickly being acknowledged in the market.

The energy scarcity situation in Europe has been the most anticipated slow moving train wreck I can think of in recent past, and it was all totally predictable. The thermal coal trade is one of those “no brainer” trades that makes me uncomfortable because it’s so easy to see coming that it almost appears too obvious, refer to the chart below:

If we’re starting out on August 10, with spot and forward thermal prices near the levels we’re at today. And ARA stockpiles are near all time highs, historically, (see below)…

…what is going to happen to coal prices as these inventories are drawn down heading into early fall? We could be talking about API2 prices of $500+ before winter weather even sets in.

Putin putting the squeeze on Europe has all sorts of negative geopolitical implications, most of which are beyond the scope of this substack. But I’d urge everyone reading this to use their imagination and widen the range of possible outcomes in your head. I found the following podcast, linked here, pretty good at asking some important questions, such as:

Will NATO survive if Europeans give in to the Russian energy squeeze?

Could the European Union fraction as a result?

These are some of the broad based questions which come up simply by scenario building thermal coal supply and demand. After doing some back channel checks recently, it seems like a political urgency is building to send fossil fuels to Europe. There is a lot a stake.

Could we be watching a world rapidly switch from castigating fossil fuels to cheering their production as Europe’s savior? This seemed quite unlikely until very recently. But as the seasons change and leaves begin falling, perhaps the winter breeze will blow in a new political zeitgeist.

However unlikely this seems, it doesn’t matter much anyway; the physics of energy won’t change with the seasons, and coal remains as the real transition fuel. I believe the next time the world goes mad due to energy abundance, it’ll probably be the result of a nuclear renaissance.

For a nuclear renaissance, the trade is NOT uranium. Its NuScale Power Corp., ticker SMR, which has been doing very well recently, see chart below. I’ve been holding SMR warrants for quite some time, which tagged their all time highs on Tuesday.

Switching gears, Fed Day on Wednesday presents yet another opportunity for J. Powell to soothe markets with his dovish words despite hawkish actions. I cannot remember the last Fed Day that was down. They’ve all been wildly bullish throughout this bear market. However, most have been selling opportunities as the rug was quickly pulled out from beneath the bulls feet after Fed Day concludes.

My equity roadmap for the week is below, and so far I’m still in the camp that we’re staging another attempt at filling ‘Gap 1’ levels above, and perhaps even staging a rally towards 4200 on the S&P 500, before the next down leg begins:

I hope we get there soon because I’m much more comfortable playing the primary trend, which is down, as opposed to the counter trend. If we get the rally drawn on the roadmap above, it will be the best shorting opportunity of this entire bear market. So keep your head on a swivel and stay agile.

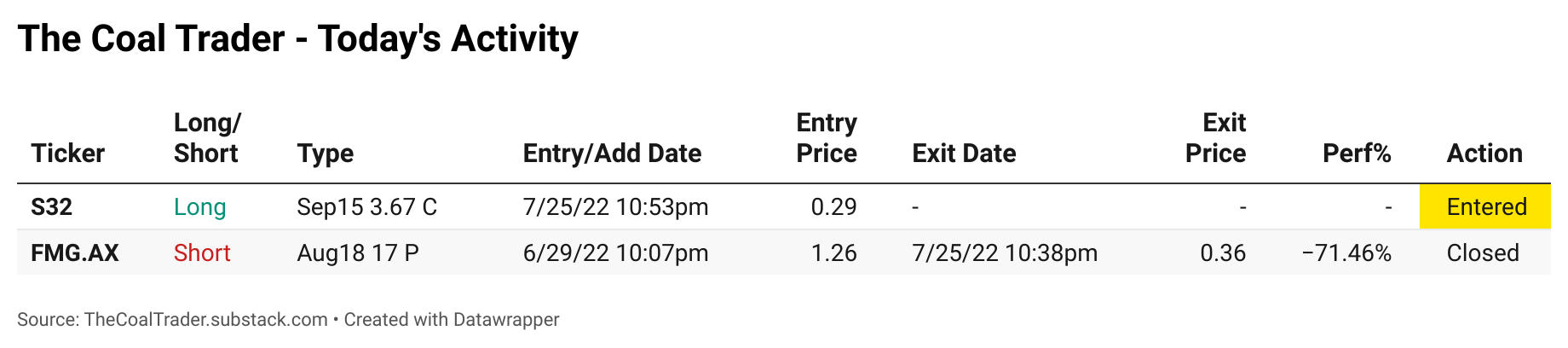

Monday’s Trading Activity: None.

Tuesday 7/26/2022

Some Glencore news is out this morning, they’ve inked a 9-month deal w/ Nippon Steel for thermal coal, see here. The international coal community has been waiting to see what kind of deal Glencore makes w/ their Japanese counterparts this year. They typically contract on an annual basis but since prices have blown out this year, neither party could agree on a price.

The $375 ton price is very close to the forward curve so it largely justifies forward futures pricing at the moment. This is an important signal to the market, the long-term forward prices for coal are very real and it’s time for utilities to pay up and sign long-term supply contracts if they want security of supply during this energy crisis.

I’m hoping to get more clarity on the long term picture and nature of long-term supply contracts during producer earnings calls in the next week or so. CEIX and ARLP could confirm what we’re seeing anecdotally in the Glencore/Nippon deal.

As I write this in the pre-market Wednesday, I’m not too concerned with Fed Day yet. What I am watching is one of my long term favorites, Thungela (TGA), breakout to all time highs. I have a note on my chart that says “All in above here” - and we’re there:

TGA is one of those names which could double again by the end of the year and it would surprise exactly nobody.

Tuesday’s Trading Activity:

Wednesday 7/27/2022

Sorry, no commentary. I was on the road travelling all day Thursday.

Wednesday’s Trading Activity:

Thursday 7/28/2022

I’m beginning to think the met coal trade is over for this cycle. I was hoping that hot-rolled coil would hold up above $900, but it’s broken down this week:

This is not good for the N. American steel producers and thus not good for US domestic met demand. There is also some negative news out of China that up expectations of Chinese infrastructure stimulus may be wishful thinking. This will not end well for met demand.

However, I do think the met lows will be much higher than we’ve seen historically. I believe the floor is approx. $175/mt for Australian PLV. Inflation is real, and costs are higher for everyone, including the Chinese coking producers which have disappointed everyone this cycle. I think their reserves are dwindling and we’re stuck with high met coal prices for the foreseeable future as a result.

The only bright spot in regards to demand is India, but I don't think they can hold global met markets up on their own. The fact natural gas is expensive is a positive - because it makes EAF expensive vs BOF - but if Chinese BOF's are unprofitable, I'm not sure it matters much.

If we're in/heading for recession, then auto demand for $60k cars is going to fall substantially, which is not good for N. American steel demand. However, steel tubular for O&G is another bright spot.

The real problem for global growth is China:

They're going through a slow-motion housing bust. It's slow because the gov't is taking over, but they cannot fix supply/demand. Therefore, construction and steel demand will probably languish for some time.

China has a demographics problem. Chinese GDP will probably pull global GDP down instead of up going forward. The rest of the developing world will have to keep growing to offset China net net from now on.

The issue w/ developing economies right now is two pronged

They're all energy importers so growth is knee-capped during this energy crisis

They have to use US Dollars to buy energy - and the US Dollar is a lot higher vs their local currency. So they're hit twice as hard on the energy front

I think the prices of everything associated (steel, met coal, etc.) will go lower, but not as low as before. Then, during the next recovery prices will go even higher than we just saw.

Another important factor is volatility. Volatility is actually a good thing if you're an incumbent met producer. There is no new competition because new projects/competitors cannot underwrite a project due to the historical volatility in met prices. So there's no new supply coming... so when we come out of the recession we'll immediately be right back into supply shortages and inelastic demand and prices will go to $1,000/mt - not being hyperbolic either.

Thursday’s Trading Activity: None.

Friday 7/29/2022

We have Pelosi traveling to Taiwan, sparking war mongering from the Chinese, yet crude oil is curiously down. Interesting right. Maybe Biden’s SPR releases are hitting the market again. Personally, I don’t think the SPR strategy will end well, but it’s probably too early to trade it. Regardless, crude oil is sitting on the edge of a cliff here and needs to bounce or the energy market factor gets sold down again with oil prices:

In coal news, Australian coal equities started the week of on the right foot, edging up Monday. Alliance Resource Partners (ARLP) announced earnings Monday morning, see here, and the results are very good. I’m looking to take profits on the ARLP calls in my portfolio, see below. I’ll then probably look for a pullback to buy into for a long term buy and hold of ARLP, using the proceeds from the successful options trade.

I’ve been working on a write-up for Morien Resources, MOX.V, over the weekend. You can expect that to hit your inbox sometime early this week. I’m also planning to develop a coal news aggregator website, so we can keep track of relevant news flow - stay tuned for that.

Friday’s Trading Activity:

For those who want to follow my trades in real time, you can always upgrade to the Founding Member tier of this Substack and get access to @TheCoalTrader private Twitter feed. Once you upgrade just send me a direct message with your email address to confirm and request to follow the private account.

Monday 7/25/2022

Tuesday 7/26/2022

Wednesday 7/27/2022

Thursday 7/28/2022

Friday 7/29/2022

Please let me know if you have any questions with regards to strategy and positioning, or anything coal related.

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or it’s Content.

Coal Trader, a massive thank you for sharing your analysis. I made huge profits on the CEIX calls, used some proceeds to buy a nice cruise vacation this fall.

In my next life, I hope I understand why WHC trades the way it does 🤔