China’s Coal-Fired Future

China’s Coal-Fired Future

From a Policy Perspective

The Policy Landscape

When studying Chinese industrial and/or energy policy, you end up running into these turn of phrases or sayings which are often repeated in a sort of short-hand way of referring to bedrock policy assumptions. They’re pretty interesting and enlightening in and of themselves which. Starting the discourse with these is therefore informative and also makes a good jumping-off point. I get the feeling there’s a catchy schtick or roll of the tongue being lost in translation on these phrases. See for yourself.

Four Revolutions and One Cooperation

“四个现代化一个共同富裕” (Sì gè xiàndàihuà yī gè gòngtóng fùyù) is a term used in Chinese policy discourse to highlight the major transformative forces shaping the world and the importance o working together on an international scale. Here’s the breakdown:

Scientific and Technological Revolution: refers to the rapid advancements in science and tech including areas of AI, biotech, quantum computing, among others. This revolution is shaping industries, economies and societies globally.

Industrial Revolution: the transformation of industries through automation, smart manufacturing, and the integration of digital tech into traditional production processes.

Energy Revolution: focuses on shifts in the global energy landscape, particularly towards cleaner and more sustainable energy sources, and advancements in energy efficiency and storage.

Green Revolution: this emphasizes the importance of environmental sustainability and ecological conservation.

“One Cooperation” means International Cooperation, and underscores the significance of global collaboration in addressing common challenges. This emphasizes the need for diplomatic, economic and technological cooperation be countries to tackle common issues and to strive for economic development.

The second turn of phrase I found throughout Chinese policy rhetoric is the following:

Three Highs and Four News

“三农三高四新” (Sān nóng sān gāo sì xīn): this one is used to refer to specific economic challenges and trends and transformations that China, as well as the global economy, is facing. It serves as a framework for policymakers to understand and address complex economic issues.

“Three Highs”

High costs and high prices: specifically costs of commodities like oil and gas which lead to higher prices for goods and services and tends to put pressure on consumers, particularly those of lower income.

High interest rates: which is often in response to high inflation.

High risks: which refers to various economic risks such as energy and food crises, or disruptions in global supply chains, etc.

“Four News”

New Changes in Economic Globalization

New Trends in Industrial and Supply Chains

New Technological Revolution and Digital Transformation

New Emphasis on Green Transformation

Okay, I realize that “policy” can be boring in and of itself so that’s all the word salad I have for now. But I think these phrases actually teach us a lot about Chinese policy and how they provide a framework for challenges and decision making. China’s policymakers are striving to collaborate with global partners and implement the latest advancements and technology in order to solve their problems and meet their needs. Chinese leadership is first and foremost fearful of inflation as well as a breakdown of supply chains. After all, they have an enormous population to feed, clothe and keep warm. A cynic with a more malevolent point of view might say “the CCP has an enormous population to control and keep happy.” But either way, they face many issues we’re familiar with and they’re actively trying to find solutions with the latest tech and innovative transformations occurring in the developed world.

2021 Energy Crisis

In a similar way that many of the ESG and “net zero” cultists have noble intentions, physics can sometimes smack you in the face with a dose of reality. This happened to Chinese policymakers during the energy crisis of 2021, which culminated in September & October of that year.

During the 13th Five-Year Plan (2016-2020), Chinese policymakers decided to implement coal supply reforms which culminated with anti-corruption campaigns and safety reforms dedicated to close smaller, more inefficient and often unsafe, mines in favor for larger operations. The overall result, whether intended or not, was a material contraction in coal production.

China's "dual control" policy, was also introduced in the 13th FYP, aimed at achieving a balance between economic development and environmental protection. The policy focused on two key aspects:

Controlling Total Energy Consumption: this aspect aimed to limit total amount of energy consumed by setting targets for energy consumption, particularly in sectors like industry, transportation, and construction.

Controlling Energy Intensity: this aimed to improve energy efficiency by controlling energy consumption per unit of economic output (GDP).

With the “dual controls” in place in early 2021, the government established a goal to achieve a 3% reduction in energy intensity over the course of the year. This target was further subdivided into provincial targets and delegated to the respective regional administrations.

However, the situation started to go awry when a strong post-Covid-19 rebound in export-oriented manufacturing led to high industrial demand and electricity consumption. Combined with the growing emphasis on limiting power usage and energy intensity, relatively low coal inventories, and rising prices of seaborne thermal coal, a fundamental supply vs demand imbalance began to take shape. Mixed signals from regional authorities and flawed domestic power pricing mechanisms eventually led to power rationing and outages. By early September a handful of localities were seeing shortages, but over 20 provinces were curbing or rationing power by October. The impact was initially on large industrial users, but even residential blackouts took place at the height of the crises. Shortages were worsened by restricted inter-regional power links and logistical challenges. Any excess capacity in one province was unlikely to be transferred to another due to "dual control" goals, concerns about potential financial losses, or simply because the necessary networks were not in operation.

The clash between market forces and state planning was at the core of the crisis.

The power outages impacted China’s overall economic growth outlook. Forecasts for GDP growth were revised down from 5% to 3.6%, and impacts to global supply chains were eventually felt. With economic growth stalling, policy makers eventually realized they needed to step-in and do something.

Policy Response

On October 8th, Premier Li Keqiang, during a State Council meeting, issued six specific directives to address the power shortages. The second directive is a noted reversal of coal supply reforms from the 13th FYP:

Ensure ample supplies for winter heating, including coal and gas, with provisions to facilitate gas transfer from south to north, as warranted.

Increase production levels at existing coal mines and expedite the operational launch of approved coal mines. Prioritize coal transportation to secure winter provisions.

Provide financial support to coal-fired generators by offering tax deferments and assistance from financial institutions.

Enhance the mechanisms for pricing coal and power through power price reforms.

Hasten the development of wind and solar energy capacity, along with emergency backup and peak-shaving power sources. Improve the emergency reserves of oil, natural gas, and coal.

Restrict the advancement of high energy consumption and emissions projects, and enhance the "dual control" mechanism.

On October 9th, Li Keqiang chaired a rare National Energy Commission meeting, concluding with a focus on stabilizing growth and implementing market-oriented energy reforms. He stressed the need to ensure energy security, improve coal efficiency, and invest in technology. Li also emphasized the importance of a gradual approach to China’s “double carbon” goals, avoiding one-size-fits-all measures.

Then, on October 12, following a State Council meeting, the NDRC announced major reforms to the coal-fired power pricing mechanisms:

Coal-fired generators must now sell power in the wholesale market, with pricing based on a 'base + float' mechanism. Renewable energy prices may remain tied to the base coal price.

Prices for coal-fired power can now fluctuate by up to 20% relative to the base price, with no upward cap for energy-intensive industries. This rule doesn't apply to the spot market.

Commercial and industrial users must buy electricity in wholesale markets, as the previous 'catalogue' tariff is cancelled. Those without a supplier will buy from the grid based on wholesale rates, with one month's notice for the switch. If they return to the grid for last-course power, they'll pay 50% more.

Residential and agricultural users are exempt and will continue with listed catalogue tariffs.

These new power pricing mechanisms are significant since they terminated the guaranteed offtake for coal power in China. This is a pivot towards market oriented pricing, with typical Chinese characteristics.

Overall, Chinese policy’s current emphasis lies in boosting supplies and expediting power pricing reforms. These efforts encompass scaling up coal production, providing financial support to coal-fired generators, and enhancing pricing mechanisms. The government aims to encourage the adoption of renewable energy, while also advocating for a cautious approach towards sudden reductions in fossil fuel usage.

These reforms have raised doubts of Chinese “Double Carbon” targets:

Achieve peak carbon before 2030

Achieve carbon neutrality before 2060

Did Li Keqiang perhaps implement a soft pivot on “Double Carbon” or simply throw the power grid and manufacturing sectors a lifeline of coal supplies? The 14th Five-Year Plan (2021-2025), which was announced on March 11, 2021 (before the energy crisis) had a particular focus on non-carbon power-generation, which appears to be in the same line of thinking as the failed “dual control” policies. We’re also already seeing opposing policy decisions, similar to coal supply reforms being scrapped. The most eye-opening example of this is the coal-power generation pipeline of approved, permitted, and/or projects currently under construction. These approvals are in direct conflict with the 14th FYP.

Coal-Power Pipeline

I’ve discussed the Chinese Coal-Power Pipeline previously in the following articles:

Power Plant Pipeline - More Thoughts - Sept. 6. 2023

Thoughts on Chinese Permitted Coal Power - Aug. 31. 2023

China Approved More Coal Power - Aug. 30, 2023

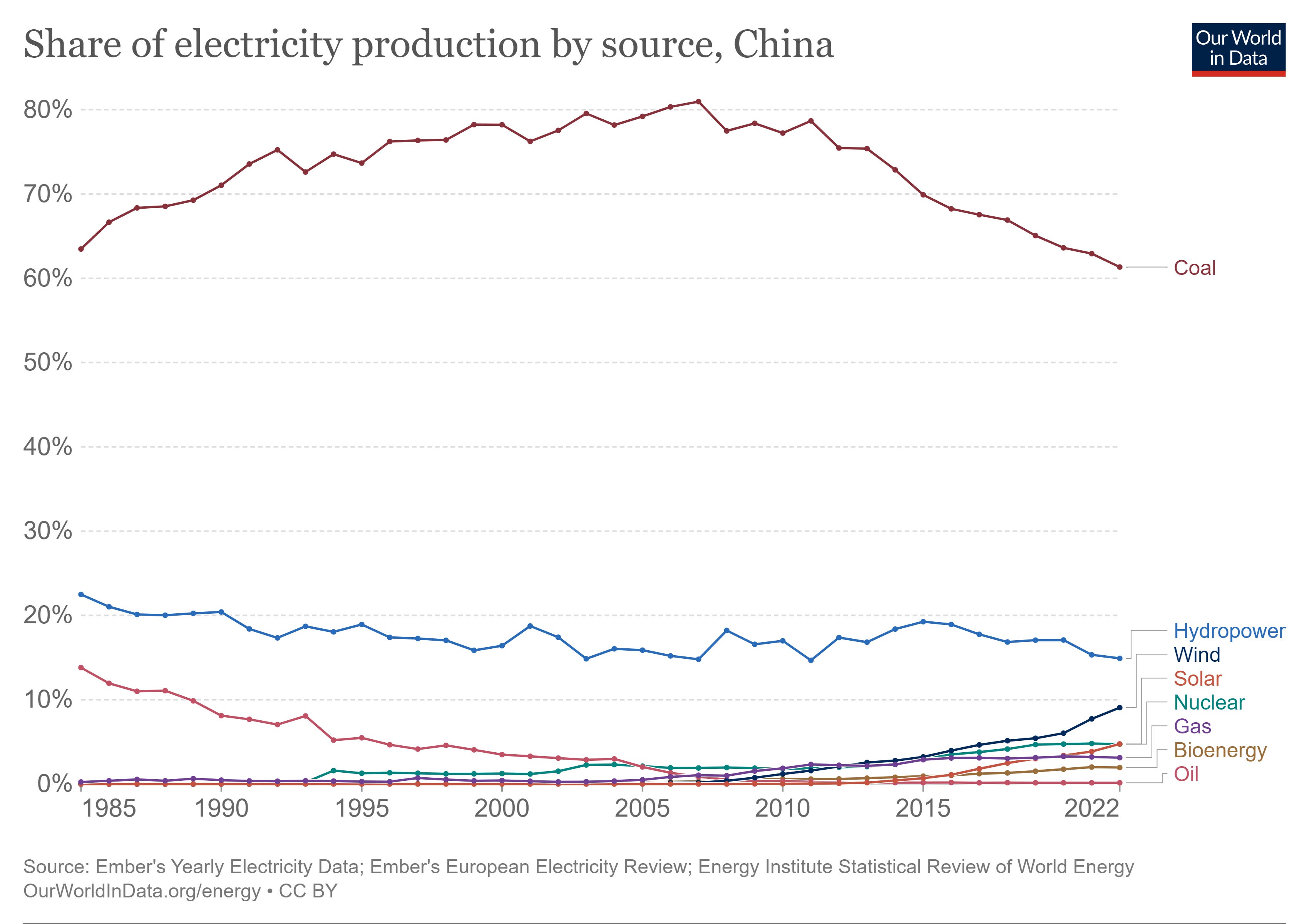

Since early 2022, there’s been 152 GW of additional coal power generation capacity permitted. This brings the cumulative capacity of plants permitted or under construction to 235 gigawatts. If completed, this would increase China's coal-burning capacity by an additional 21%. It’s hard to fathom the following plot of coal’s share of power production continuing to decline when coal-gen capacity is increasing 23%. But for coal demand to increase, you only need coal’s share to more or less flatline as total electricity production grows.

To be fair, China has also been building a massive amount of renewable capacity. The IEA estimates that between 2019 and 2024, China will account for 40% of global renewable capacity expansion.

But given the “Double Carbon” goals, why are they continuing to also buildout all of this coal-fired capacity?

Potential Answers…

After discussing it a bit with David Fishman, there’s a few potential answers, or a combination thereof, which may explain the continued buildout of excess coal-fired capacity:

For regions that are currently net power importers, there are regulation mandated reserve power capacity levels which they must eventually meet. These regions may have to build coal-gen capacity if there’s no other source types available (if solar/wind are not feasible, for example). This is particularly critical for regions that rely on hydropower since historical hydropower generation has been extremely volatile due to prevailing weather patterns and is primarily backed by increased coal-gen.

David believes utilities are preparing for a future intermittent-heavy grid due to the material development of solar and wind capacity in recent years. China is planning on using coal-generation to load follow, i.e., ramp up and down in response to intermittency of solar and wind. In the developed world, particularly the US, we’ve seen renewable backup come primarily from natural gas-fired “peaker plants” which are ramped up and down in response to solar/wind.

The third reason is less policy-driven, but some regions have decided to boost local GDP by investing in easy infrastructure projects like coal fired power plants in the last few years that such projects will be “allowed” to be built. This assumes the first “Double Carbon” goal, the 2030 carbon peak, will be accompanied with a ban on new coal generation projects.

In general it seems like the continued coal project buildout is part insurance policy to backup volatile hydropower and part insurance policy to backup volatile renewable energy. Energy security is the new priority as opposed to rushing into aggressive decarbonization goals.

You can read more of David Fishman’s thoughts on The China Project, linked here. His latest piece China is going to use less coal, despite reports to the contrary is from Sept. 21, 2023. You may have to create a free account to read the article.

Where Consensus is Wrong

The consensus for coal’s future in China seems to hinge on power demand peaking in the next few years. They believe lower power demand combined with heavy penetrations of renewables will cause coal demand to peak far ahead of the “Dual Carbon” goal of 2030. Most analysts use the real estate and construction downturn to point to lower future industrial power demand. But as we’ve seen so far in 2023, that type of analysis is extremely flawed. Despite the real estate and construction bust in China over the past two years, power demand continues to grow at a healthy clip (up 3% for Jan-Aug 2023 YoY). Similarly, even steel production continues growing despite the real estate bust.

China has reached the scale where 3% long-term CAGR’s are very meaningful to future raw material supply/demand forecasts. In terms of scale, China’s total power consumption surpassed the US’s in 2010 and now uses twice as much power as the USA. They added an entire USA worth of power demand in 13 years! You can see the growth by source in the chart below:

The reason power and steel demand continue growing is that China is the world’s manufacturing hub. They are not only supplying developed markets with finished goods, they’re also supplying emerging markets with finished goods, and emerging market populations continue growing and rapidly increasing their standards of living. The manufacturing footprint in China therefore continues to grow, and power demand will continue to grow as a result.

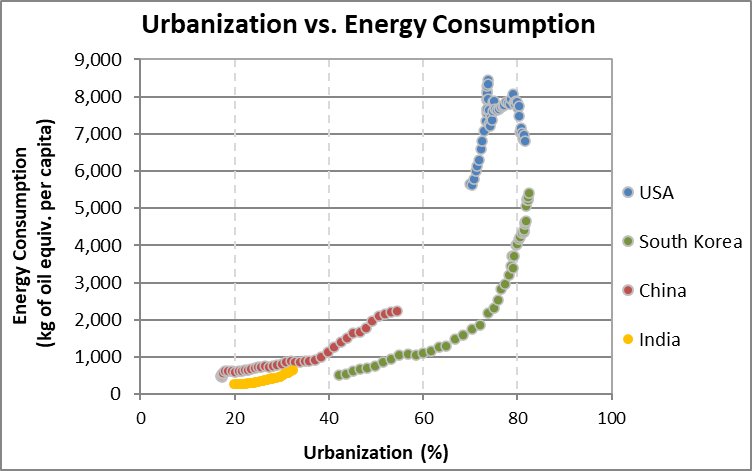

Residential power demand should also continue to rise as the standard of living for Chinese citizens approaches Western levels. Power consumption does not typically plateau while a country is in the exponentially rising part of their S-Curve, refer below:

Industrial power demand may not grow at 8-9% per year like it did a decade ago, but 3-5% at China’s scale is very meaningful. As power consumption rises every year, China will need to match that growth with new renewable generation growth, otherwise the utilization of the coal fleet will grow, driving up coal demand. China will therefore run the same risk the developed world is dealing with as their grid becomes reliant on intermittent sources, and Europe’s woes in particular come to mind.

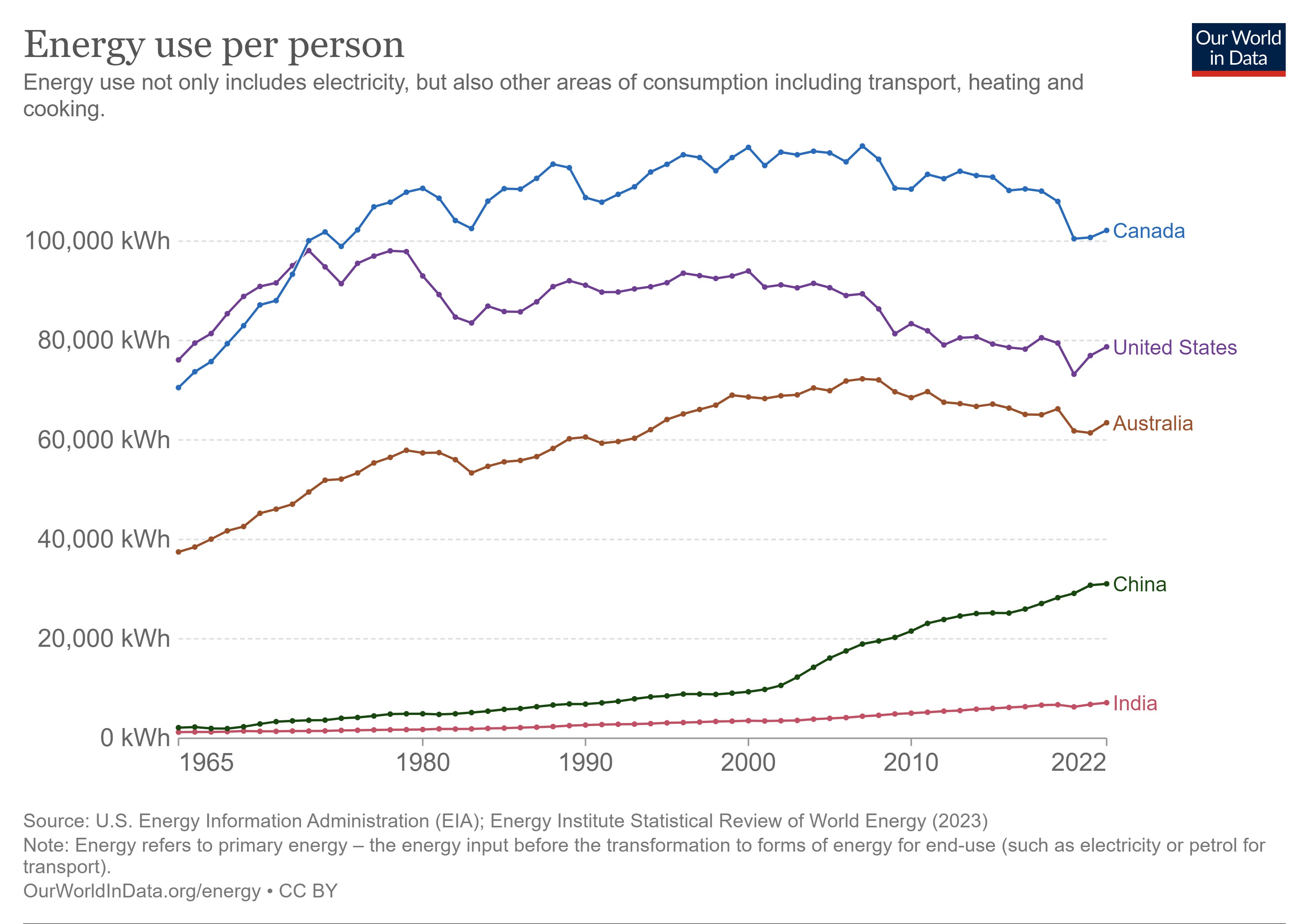

You can peruse each country’s per capita energy consumption on the following map. Try to envision China’s energy consumption plateauing while the following takes place:

They continue manufacturing most of the world’s finished goods,

While their population’s living standards continue to grow, and

As their transportation sector increasingly leans on the power grid for energy, as we’ll see in the next section.

It’s an incredible naive notion.

https://ourworldindata.org/grapher/per-capita-energy-use

The second area consensus seems to be wrong is in the belief that older less efficient plants are going to soon be retired as the new coal-gen pipeline is constructed. Chinese coal plants are not that old and it makes very little sense to build new capacity just to retire old capacity. From what I’ve read, the current fleet is fairly modern and meets the very stringent emissions standards which Chinese policymakers have put in place.

The EV/NEV Kicker

There’s another term often used in China, "煤多气少油缺" (méi duō qì shǎo yóu quē), which can be translated as "abundant in coal, scarce in gas, lacking in oil." This is an acknowledgement of being rich in coal but lacking in abundant natural gas and oil resources. Chinese dependence on foreign crude oil imports is a national risk. With rising geopolitical tensions, it makes a lot of sense to hedge that risk, which can of course be done with coal. About one-third of China’s crude oil consumption goes towards transportation. This can be mitigated by powering the transportation system with the electric power grid.

New Energy Vehicle (NEV), is a term commonly used in China to refer to vehicles that use non-traditional sources of energy for propulsion. This includes electric vehicles (EVs), plug-in hybrid electric vehicles (PHEVs), and fuel cell vehicles (FCVs). Benefiting from a 10% vehicle purchase tax exemption, as well as China’s burgeoning domestic automotive industry, NEV’s now account for 37% of sales in China. By putting the transportation energy demand burden onto the electric power grid, total power demand will surely continue rising rapidly.

Napkin Modeling Chinese Power

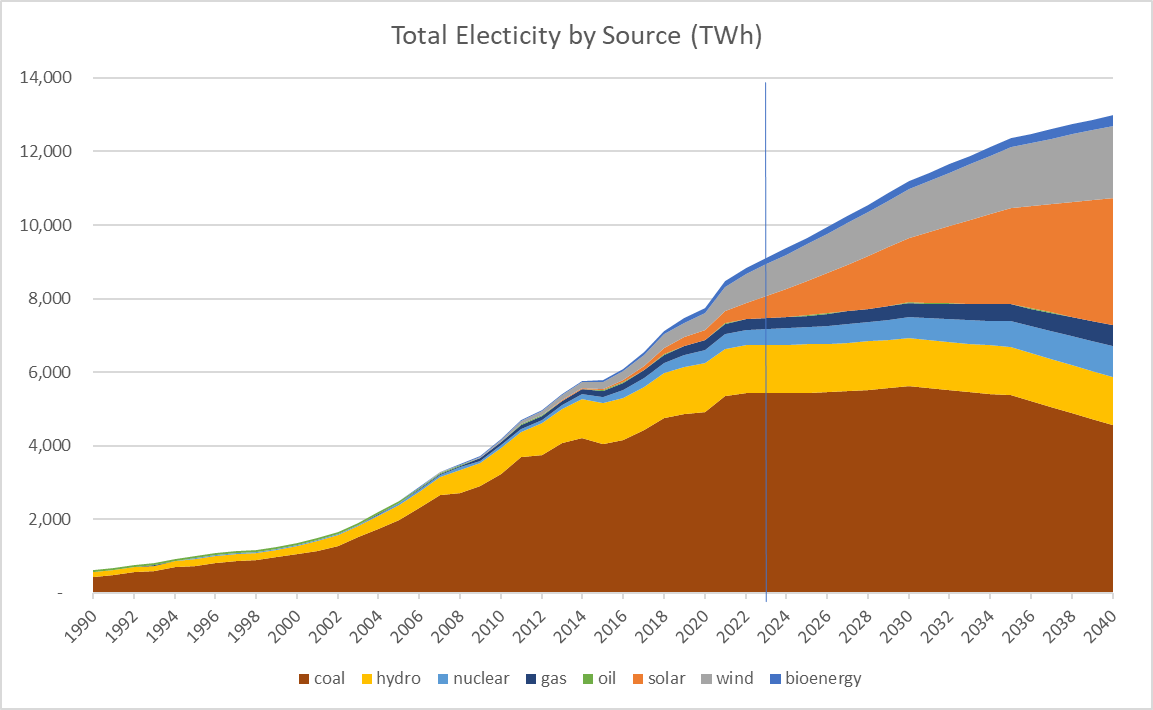

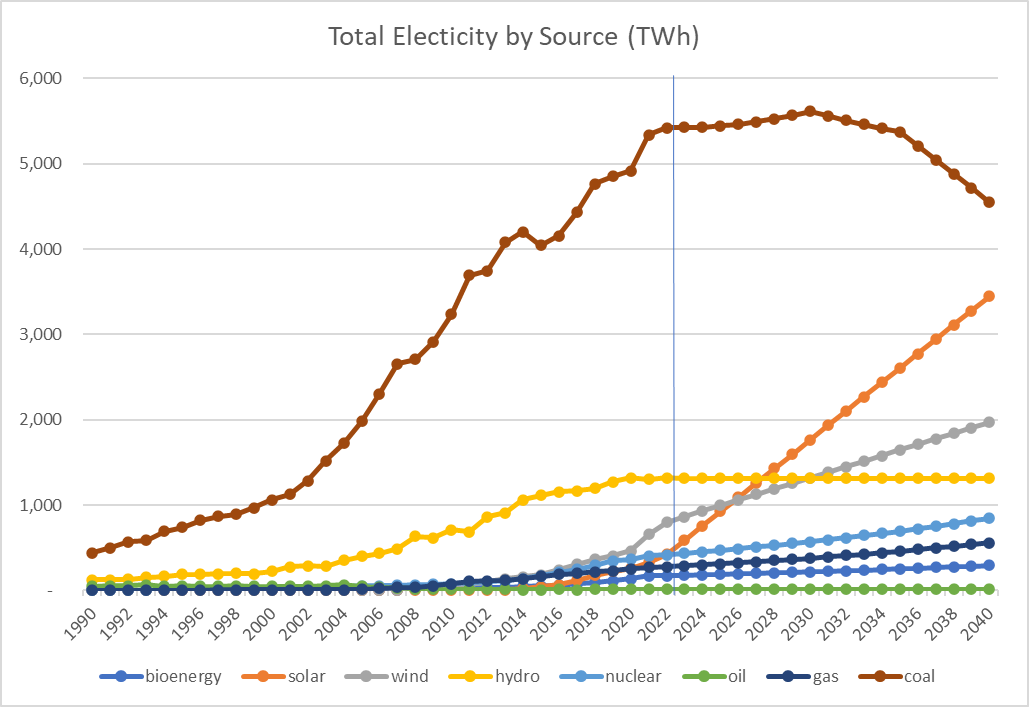

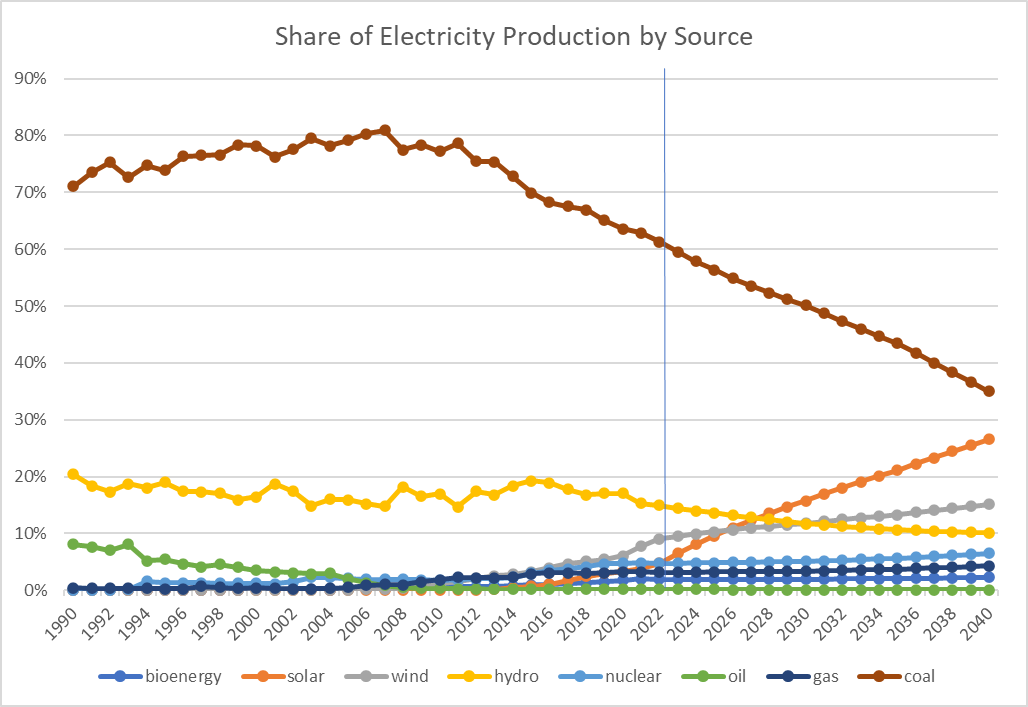

Now that we’ve have a sense of what’s going on in terms of policy and future growth, lets put some numbers together in order to visualize the net effect. I’ve made a simplified, back of the napkin, model of total Chinese electricity production, by source, with the following assumptions:

Total power demand growth of 3% from 2023-2030, 2% from 2031-2035, and 1% from 2036-2040.

This assumption appears rather conservative if we compare the those figures with the average growth rate from 2016-2023 of 5.85%.

Wind-generation growth held flat at 65 TWh per year from 2023-2040.

In the wake of the offshore wind project subsidy, which was phased out in 2020 and 2021, growth from wind should decelerate from the growth period of 2021 and 2022. In 2021 and 2022, incremental wind-generation was 189 TWh and 145 TWh, representing growth rates of 41% and 22%, respectively. I think 65 TWh of continued growth per year is a rather aggressive assumption, but I’d like to be conservative here and keep things very simple.

The result is wind-generation growth at 5% CAGR, and total wind-generation as a share of China’s total-generation, growing from 9% in 2022 to 15% in 2040.

Solar-generation growth held flat at 168 TWh per year from 2023-2040.

This may not sound aggressive but I believe it is. Incremental growth of 168 TWh in 2023 represents a 40% increase year over year. I’ve then held that figure flat for 17 additional years. This 40% jump far exceeds the solar-generation growth of 66 TWh and 93 TWh, representing growth rates of 26% and 29% in 2021 and 2022, respectively.

The result is solar-generation growth at 13% CAGR, and total solar-generation as a share of China’s total-generation, growing from 5% in 2022 to 27% in 2040. Please note that for solar penetration to reach this share of the total, some form of grid-level storage is being baked-in to these assumptions as well.

Flat hydropower-generation at the past three year average.

Nuclear-generation growth at 4% annually through 2040.

Gas-generation growth at 4% annually through 2040.

Bioenergy-generation growth at 3% annually through 2040.

Flat oil-generation at 2022’s figure.

Coal-generation then gets whatever is leftover in terms of the gap between total electricity demand and the net result of generation from all other sources.

The following charts represent the modeled results:

To be honest, I find the modeled growth and resulting penetration of solar and wind to be quite aggressive, with a combined share by 2040 representing 42% of total generation. This result would be quite the feat and definitely worthy of applause. An interesting result in this model is that coal generation peaks in 2030, which just happens to line up with the first “Double Carbon” goal.

This model demonstrates that if total Chinese power demand continues to grow modestly, China will need to continue supplying coal at greater than or equal to current levels for the next 15 years or so. Even though coals modeled share of total generation drops from 61% in 2022 to 35% in 2040, coal consumption will nevertheless remain above 2017 levels.

Summary

I think it’s important to think about Chinese policy and ask ourselves why their actions don’t quite line up with their rhetoric. They’ve stated the “Double Carbon” goals and attempted supply side reforms to the coal industry, but they immediately ran into trouble when power reforms collided with potential economic growth during the 2021 energy crises. In the end, economic growth and stability will win-out in the policy tug of war every time. Energy security is China’s primary goal.

China is very serious about expanding renewable energy, but they’re also serious about hedging volatile hydropower output and providing stable backup to intermittent wind and solar. China is not heading down the path of Europe, which is going “green” at the expense of hallowing out their manufacturing capacity. China instead is increasing capacity of all sources of energy and plans on maintaining a manufacturing competitive advantage by using their cheap and plentiful coal reserves.

In a follow-up article, I’ll dig deeper into China as well as India’s coal-generation pipeline. I will try to figure out the incremental seaborne thermal coal demand forecast by pulling apart the combustion technologies of the coal utilities being constructed and making some assumptions in terms of domestically sourced vs import sourced coal supply requirements.

Please let me know if you have any questions with regards to strategy and positioning, or anything coal related. I try to answer every question.

For those who want more coal analysis and content, you can check out my website here. I’m still developing some features but many have already made the move over to the thecoaltrader.com.

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or its Content.

Really insightful piece. This really helps me frame how the demand situation looks in China. Looking forward to see your follow up and especially a similar piece on India

Speaking of China:

Almost all metal prices down today, yet nearly all (base) metals and mining related stocks in Europe up big. I'm guessing because of this news:

https://www.reuters.com/markets/commodities/eu-plans-anti-subsidy-probe-into-chinese-steelmakers-ft-2023-10-10/

Or am I missing something else? Any thoughts on this? Big news or rather a storm in a glass of water (stocks seem to be coming back down already at the moment :)? And depending on how this pans out, who might be the biggest winners or loosers?