Trading Peabody's Rally (BTU)

Trading Peabody's Rally (BTU)

Chase Strength or Wait for a Pullback?

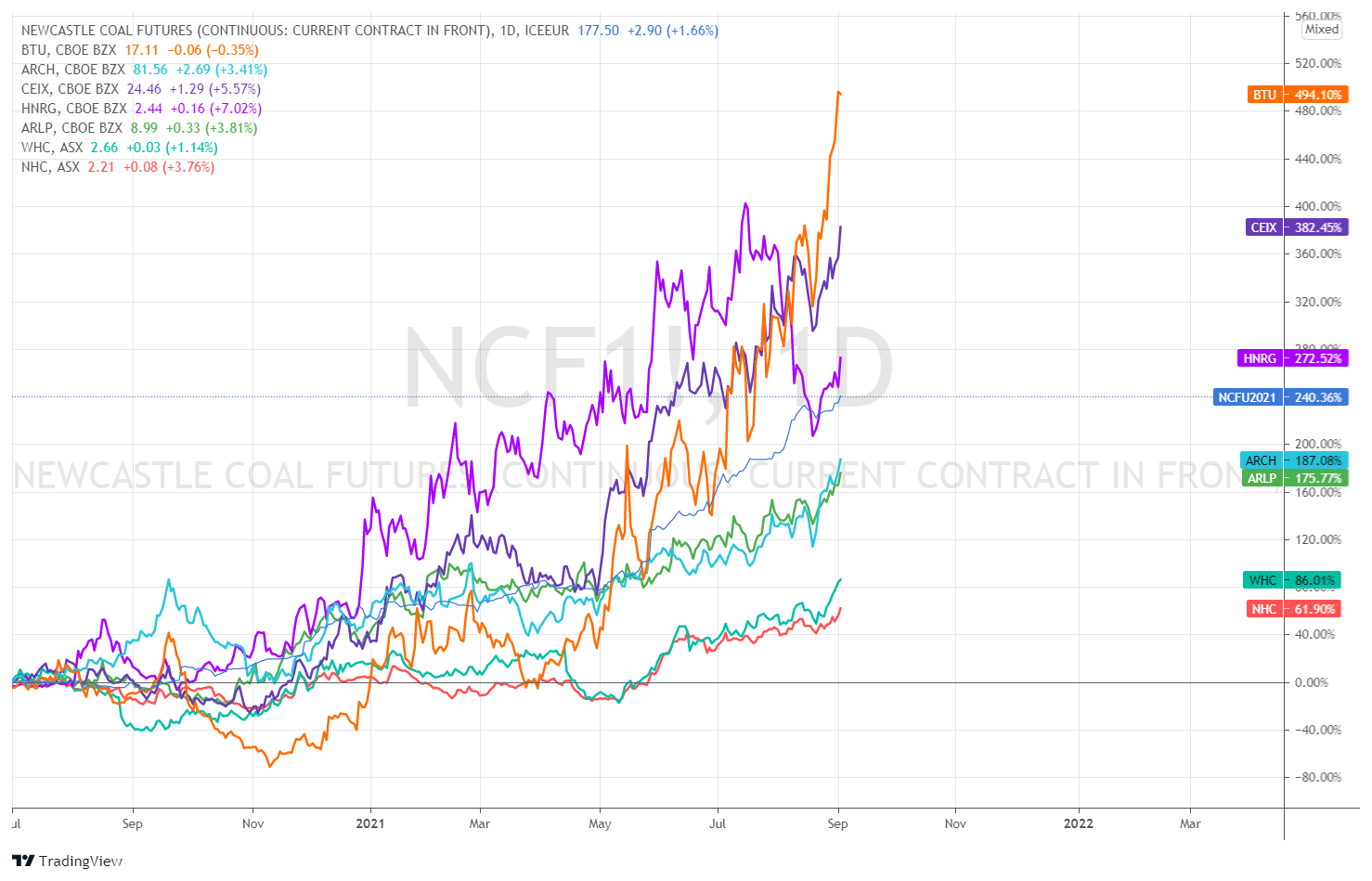

Peabody Energy (BTU) is on a tear. It has demonstrated a remarkable amount of volatility these past few months and has outperformed every other thermal coal name across most time frames incorporating the second half of 2020 and 2021 ytd:

Market Cap

As with anything in the markets, large pools of institutional capital and they’re associated fund flows drive performance. It’s not small retail traders pushing BTU, or any other name for that matter higher, it’s the big boys. The big boys need liquidity and that’s typically found in companies with larger market capitalization.

Let’s compare market caps, according Yahoo! Finance:

Whitehave Coal (WHC.AX) $2.933 Billion

Peabody (BTU) $2.004 Billion

New Hope Coal (NHC.AX) $1.881 Billion

Arch Resources (ARCH) $1.251 Billion

Alliance Resources (ARLP) $1.159 Billion

CONSOL Energy (CEIX) $840 Million

Thungela Resources (TGA.L) $446 Million

Hallador Energy (HNRG) $72 Million

You’ll notice that I’ve excluded Exxaro Resources, PT Adaro Energy and Thungela Resources; these aren’t on the hit list with US based institutions. You can also probably exclude Whitehaven and New Hope on the same parameters. That leaves the big boys with only a few options if they need a thermal coal allocation. There’s Peabody w/ a $2 billion market cap, and Arch with $1.25 billion. ARCH doesn’t really even consider themselves a thermal producer (even though they have a material ownership in PRB assets). Therefore, BTU is the only real option for US-based institutional sized capital to safely get a quick thermal coal allocation.

The fact that CONSOL’s market cap is under a billion dollars is astounding to me, but that’s a side note. If you want to learn more about CEIX, I wrote an article here.

Asset Profile

I have not written a deep dive on Peabody yet, but from a competitive advantage standpoint (which I talk about A LOT) they are a very mixed-bag. The PRB assets are great mines; they’re high volume, low cost, produce from the thickest coal seams you’ll ever see, and with oceans of reserves what’s not to like? Well, they’re landlocked and generally cannot access the ocean to be exported (although a small bit trickles out). Even if PRB coal could be exported in size, it’s not apparent to me that it would be economic, under most historical conditions anyway. The coal has a low heat content so it doesn’t travel very well abroad. It does travel domestically within the US simply because of very favorable freight rates thanks to the monopolistic rail industry, serviced by Warren Buffet’s BNSF and also Union Pacific, ticker UP.

The problem is the US domestic power generation market is in terminal decline; the US won’t be burning coal by 2030 so these mines are dead, right? Well that was the consensus only 12 months ago. Now that natural gas is proving to be an expensive “bridge fuel” the world is slowly coming around to the fact they rely more on coal than perhaps they thought. I’m pleasantly enjoying watching the abundance mindset created by a decade of cheap natural gas, get wiped clean from policy makers mindsets. Let’s hope it continues.

Peabody of course also has good Australian assets and some metallurgical assets (which have not been performing), but we’ll save that discussion for another day.

In terms of assets with superior competitive advantage with the potential for long term performance (i.e., not go bankrupt) in any climate, I think you have to give the nod to CONSOL. First of all they have not gone bankrupt, whereas Peabody has, and they weren’t really close to going bankrupt a second time in late 2020, whereas BTU was. That’s because CONSOL had the assets which provided the ability to pivot from a mostly domestic based sales blend into electricity generation markets, to a mostly export sales blend incorporating various markets including petcoke, which made up 42% of CEIX’s sales in Q2 2021.

Despite these fundamental shortcomings, relative to their peers, Peabody is getting all the attention. I forget who said it first, but Peabody is basically the “coal-coin” for this stage in the cycle. Which is appropriate for the meme-inspired backwards logic of the current investment landscape.

The Trade

Stop waiting for a pullback. In this market where coal equities are rapidly chasing fundamentals higher, you may not get the pullback you’re expecting. Moreover, if everyone is sitting around waiting for a pullback, that very feature will prevent one from occurring.

I maintain the mantra “Chase Strength”. you have to chase strength because the strength is simply affirming the improving fundamental thesis.

We are in the exponential stage of the rally. So either decide that you want to participate, and get it, or decide that you’re ok with missing out. Either way is fine, everyone has their own risk tolerances.

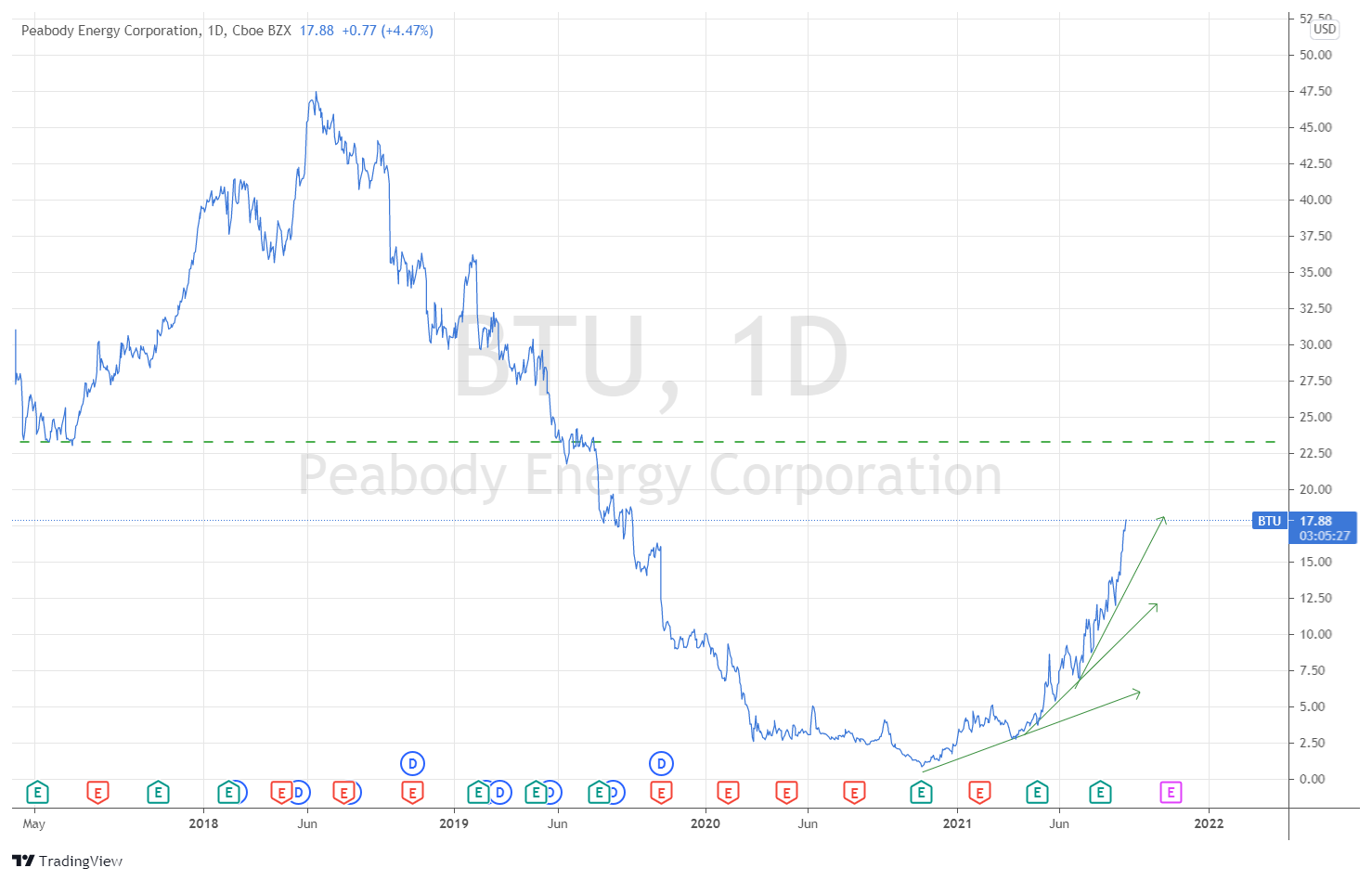

The following chart is how I see it today:

That green-dashed horizontal line is right around $23. I think BTU is destined to trade into the $20-23 range. I believe it’s a very high probability trade that I’d handicap it at approximately 80% odds of occurring. I think you can also put in a stop loss around $16 per share. Now we have a risk range and a probability.

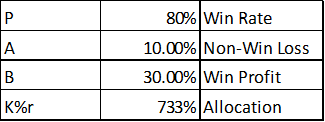

From here I like to judge whether we have a good risk vs. reward trade by employing the Kelly Criterion. I plugged the Kelly formula into excel and put in the odds at 80% for win rate, the percent profit from if I’m correct (30%), and the percent loss if I’m incorrect (10%). I’m using $23 as a win target, and $16 as a non-win stop loss target:

The K% is the allocation to each bet with the above assumed estimated statistical criterion. If the allocation is positive you should take the bet. If it is over 100% it means you should add leverage. I don’t take this allocation number verbatim and apply it to my trading, I simply use it as a measuring stick.

I also like to utilize options on something with this type of risk vs reward. However, the implied volatility on BTU options is really high. January at the money calls are currently trading at 95 IV, for example. When it’s that high I usually try to avoid them. Owning the common shares provides you with option-like returns anyway.

Summary

So there you have it. BTU is not the best thermal company available today in terms of it’s fundamentals and asset base. But it is the popular one with all the momentum, probably due to institutional sized capital flows looking for a quick way to get coal exposure.

You can wait to get in on a dip, if one ever occurs, or you can play the risk vs. reward trade I outlined above. Everyone has their own risk tolerances and you should access your what yours is when it comes to “dodgy” coal equities! However, I’ve outlined how I am framing the situation and defining my own risk, and I’ve demonstrated how to use the Kelly Criterion to quantify whether the risk vs reward warrants pulling the trigger for my own account.

If you found this write up valuable please smash the like button below and if you have any questions please free to ask. I find all feedback helpful.

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or it’s Content.

All of this continuing strength makes me really want to reallocate to an even higher allocation of coal in my portfolio, which is already about 20%. The rest is steel, shipping, some oil/gas. But man... no one is seeing coal coming and that makes it even more attractive to me.

Great write up. Just with WHC and NHC those market caps are in AUD and not USD.