Q1 2023 Earnings Review

Quarterly highlights along with my thoughts on each company

The following is a Q1 Earnings Review for each of the US coal producers that have announced so far. These include:

Arch Resources

CONSOL Energy

Alliance Resource Partners

Warrior Met Coal

Ramaco Resources

Peabody Energy

This review quickly summarizes each company’s quarter and earnings highlights, along with a visual of the balance sheet. Then I conclude with my thoughts on each company.

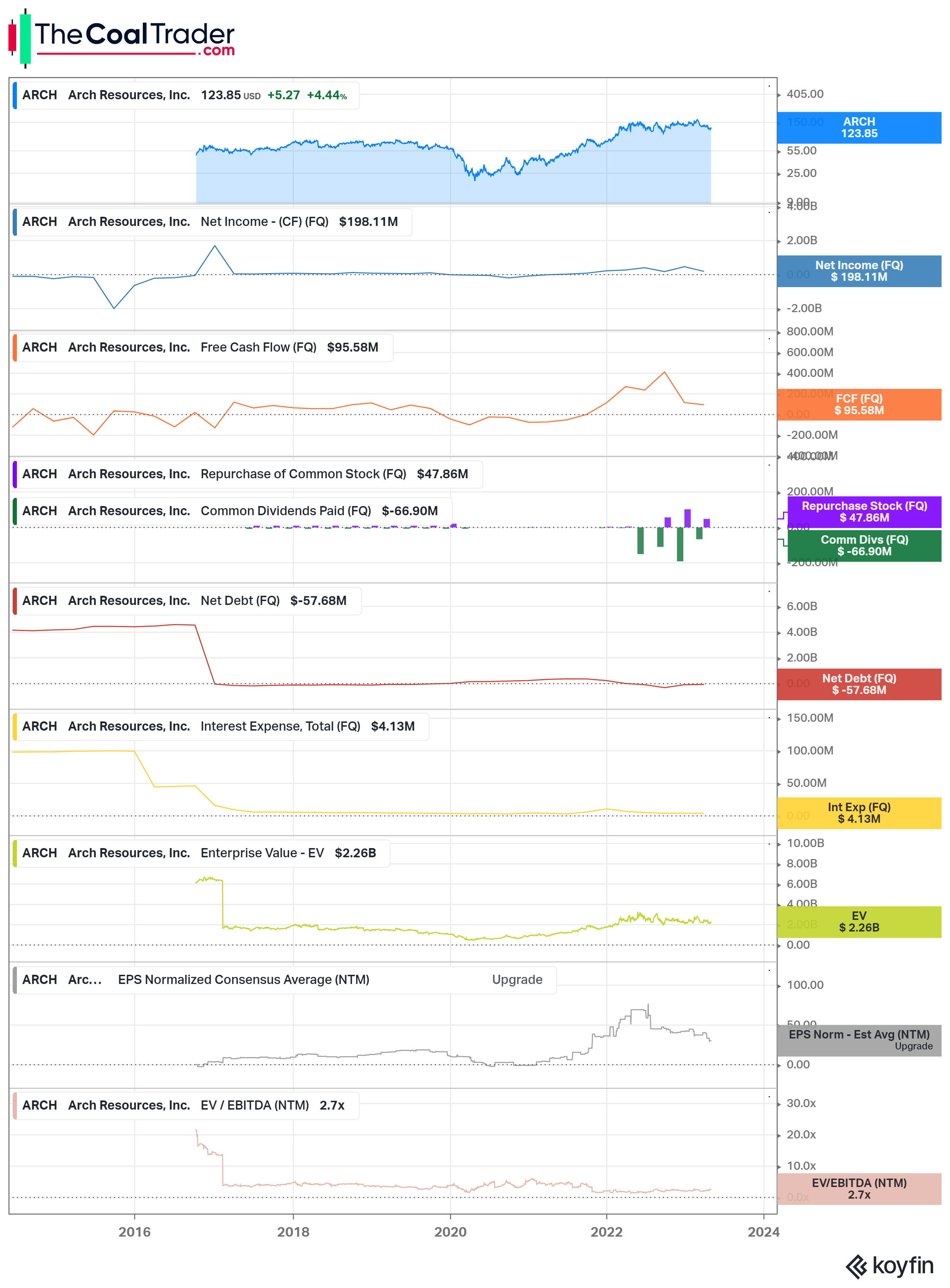

Arch Resources

Arch Resources (ARCH) reported a strong Q1 in its Met Coal segment, driven by increased production at Leer South which led to higher sales volume and lower cash costs. However, a decline in world markets is expected to reduce Q2 realizations. Domestic met fixed price sales commitments also rose. The thermal coal outlook weakened due to geological issues at West Elk and weak demand, with up to 1.0 million tons of output expected to be cut for 2023. Customers are also looking to defer deliveries of contracted PRB coal, with 5% expected to be pushed into 2024.

Earnings Highlights:

Q1 metallurgical segment generated an EBITDA contribution of $263 million.

The price of met coal surged QoQ to $209.84/ton, driven by high export prices.

Sales of metallurgical coal increased by 40% YoY to 2.2 million tons as Leer South production approached full capacity.

The metallurgical segments cost performance during out at $82.66 per ton despite inflationary pressures, marking Arch's best cost performance in the past six quarters.

Leer South's productivity gains and volume growth are expected to result in another step up in volumes in 2024, and Arch reiterated its cost guidance of $84 per ton at the midpoint for full-year 2023.

The thermal segment generated $46.3 million in segment level EBITDA

Price of Other Thermal coal (PRB and CO) dropped to $18.49/ton as a result of a smaller proportion of West Elk coal in the average sales mix.

Sales volumes of Other Thermal decreased YoY due to limitations in PRB rail service, which are gradually improving, and geological challenges at West Elk.

My thoughts on Arch:

Despite lower met sales and higher QoQ price associated costs, Arch managed to lower overall met cash costs per ton. That’s not really an easy feat but they managed to accomplish it by having both Leer and Leer South run effectively without any hiccups. This is an important development for Leer South, which is finally getting up to its nameplate capacity and operating at a level Arch believes will be the norm going forward.

From the cost side, Arch looks very favorable compared to their peers and should be the low cost met producer in the US for the foreseeable future with the exception of perhaps Warrior Met as the mines in Alabama increase production and get back to nameplate capacity.

Arch continues to deliver material shareholder returns in the form of dividends and buybacks, in addition to repurchasing convertible securities which reduces future dilution. Arch is now the classic “grandpa” stock of the sector. They should be able to perform consistently at the bottom quartile of the cost curve and provide meaningful returns to shareholders going forward, almost despite what the overall market throws at them. Arch is a buy and hold if you don’t want to think too hard about coal supply/demand and/or management’s future decision making.