Portfolio Weightings & Performance

Portfolio Weightings & Performance

Daily Commentary & Positioning - Week of May 2, 2022

The following is daily commentary for the Week of May 2, 2022. You can scroll down to see portfolio positioning throughout the week along with various performance metrics. This post gets updated every morning prior to market opening so be sure to check back for daily updates.

Monday 5/2/2022

This week seems pivotal for broad equity indexes, bonds, and the US Dollar. The US Dollar has been screaming higher along with bond yields, and equities had a terrible April. This week is Fed Week of course and it has the potential to either mark a local maximum for these trends, leading to a bounce in equities and bonds, or providing a trap door release, sending them both puking lower.

It will all come down to the Fed’s forward guidance. The 50 bps hike is a given now but the market reaction will all come down to whether or not Powell and company turn dovish on the length and/or magnitude of future hikes. If they hint of an early pivot equities will react positively, if they do not hint of a pivot at all equities will react negatively.

The inflation narrative seems to have peaked, with many pundits calling for 2-4% CPI over the next 12 months (still positive but decelerating). Could this mean the inflation trade is about to unwind? If a recession (negative growth) gets priced-in by markets, I think the inflation trade will also selloff, at least modestly.

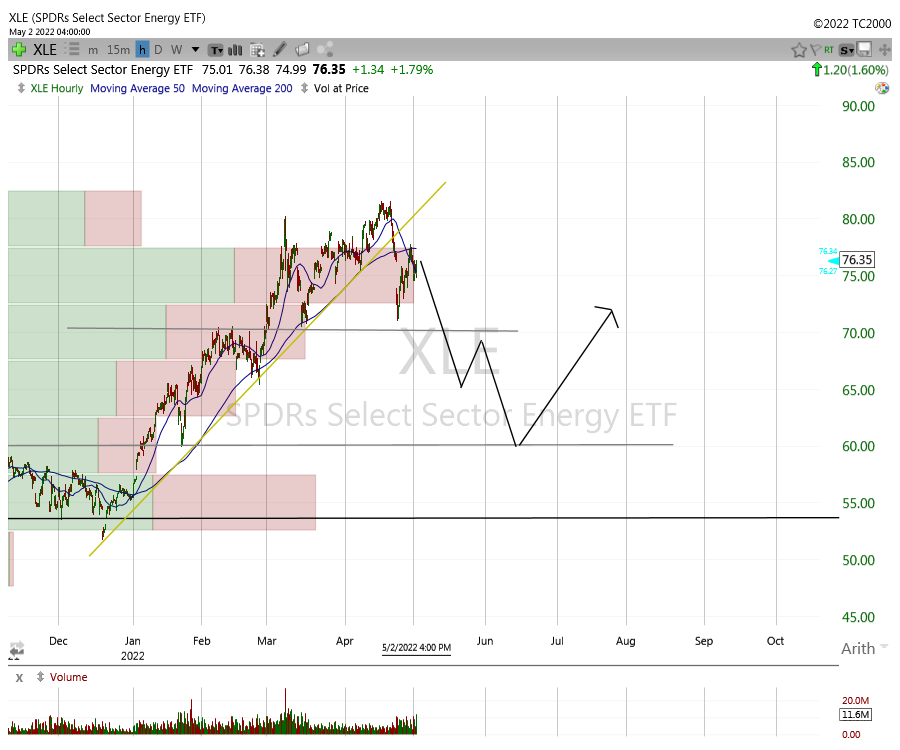

I have been watching the oil and gas equities very closely and I eventually want to invest approximately 20-30% of capital into the sector. So far I only have a ~5% allocation to VAL warrants, which gives me some juice, but I want to spread another 20-25% among a handful of names, mainly service and drilling companies. I’m waiting on the potential inflation trade unwind to occur before plowing the capital into oil and gas services. This is what I’m worried about:

I’m also using the OIH as a proxy to time the entry, but it looks very similar to the XLE above.

The US Dollar as I mentioned earlier is screaming higher, and I think it will continue higher as the only safe-haven trade on the board. This is Brent Johnson’s Dollar Milkshake Theory playing out before our very eyes:

As rates tighten the grip on economic growth, and as markets selloff in kind, I believe Powell will eventually pivot - sometime this summer.

The pivot could perhaps be some form of Yield Curve Control (YCC) or a termination of QT, or some other manner of appeasing markets. But the result will be an unwind of the US Dollar safe-haven trade and a resumption of the commodity bull market. That’s when I want to be max long mining resources and oil and gas service companies.

To reiterate the plan:

Aggressively hedge into the summertime selloff (tactical tech puts)

Enter O&G service equities in anticipation of Fed pivot

Hold coal equities for the long haul as shareholder return policies ramp-up

In terms of coal equities, I tweeted the other day that coal investors should stick to companies which are implementing shareholder return policies. In terms of WHC, you can see their “Notification of buy-back” updates here. The companies that cannot yet return capital to shareholders will be more susceptible to the inflation trade unwind I mentioned earlier. The following producers meet this criteria:

WHC - Thermal

ARCH - Met & Thermal

TGA - Thermal

NHC - Themal

AMR - Met

HCC - Met

ARLP also meets the criteria but Joe Craft is busy investing for growth in non-fossil and I think I’d prefer to implement that sort of hedge myself in my own portfolio. Sorry Joe. BTU is a long way from shareholder returns due to credit and surety bond covenants. So stick with those listed above, unless you want to go down the quality scale and play some of the smaller names. But I’ll leave that topic for another day.

In terms of coal’s long term fundamentals, I’ll leave you with the following Tweet from Twain’s Mustache:

The point is the following:

Coal demand will not plateau until the 2040’s, yet every coal producer on the planet has re-rated as if the industry will be dead in 5 years.

A massive re-rate will occur OR massive shareholder returns, roughly equivalent to a re-rate, will occur. Therefore, to be on the safe side you need to hold those companies with shareholder return policies for the duration of this cycle. And since there’s almost no material incremental supply planned in the near term future, this cycle is just getting started.

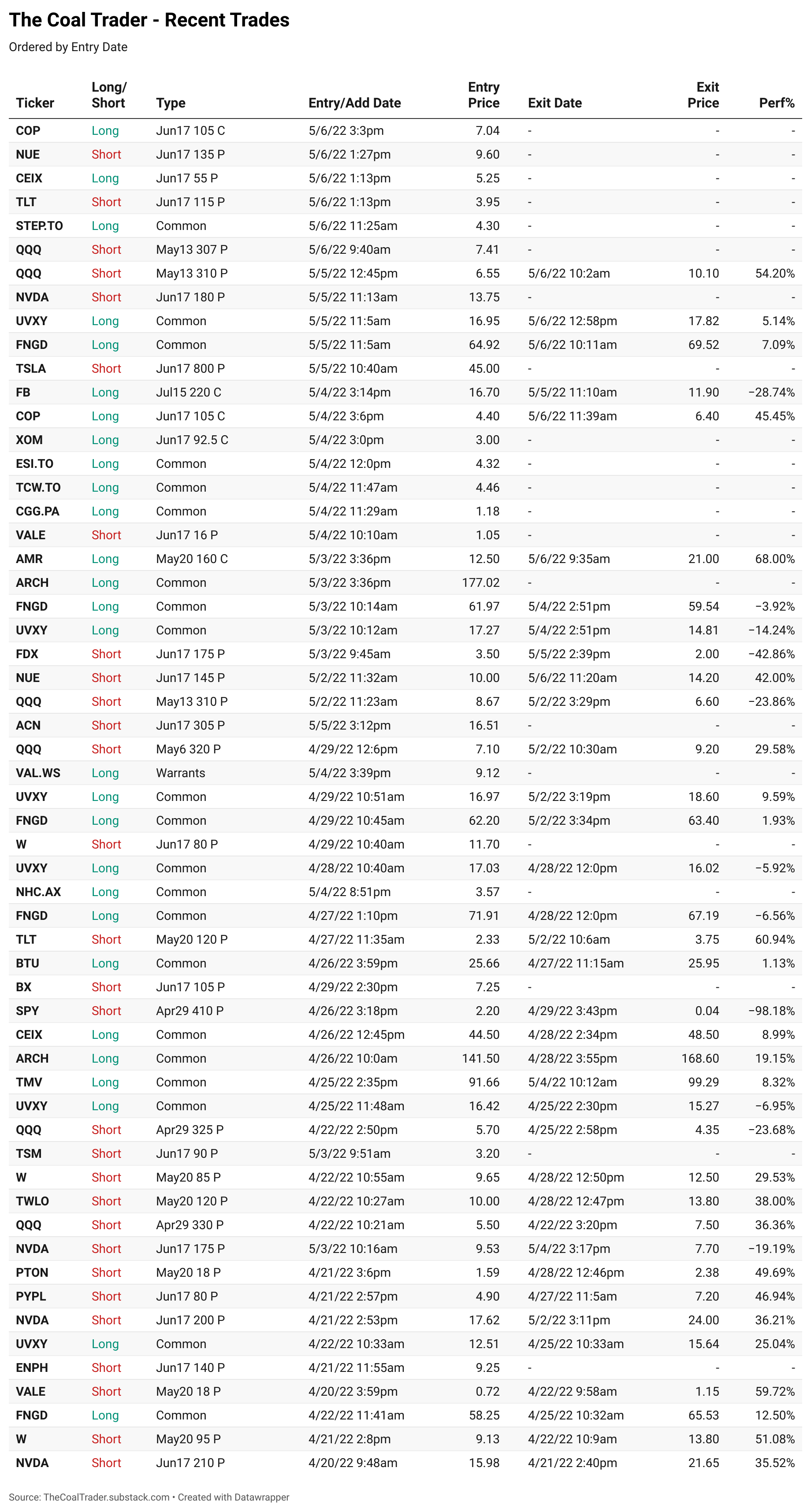

Monday’s Trading Activity:

Tuesday 5/3/2022

There is a significant risk to the game plan laid out in Monday’s commentary. I could be simply wrong in my expectation of XLE/OIH and crude oil weakness associated with an inflation trade unwind. I try to do my best to let price dictate my reality and right now the price of XLE/OIH is suggesting my pullback thesis is incorrect. If I look at copper prices, the inflation pullback IS occurring:

But crude oil and it’s various proxies are not really pulling back:

To hedge my own anticipation of a crude oil pullback being incorrect, I’m already holding a 4-5% position in VAL warrants. But if XLE/OIH continue to display relative strength I may have to start nibbling on additional O&G service exposure sooner than anticipated.

If you think about a near term stagflationary future, it would make sense for crude oil prices to consolidate recent gains instead of pulling back in the face of lower growth forward estimates. But you’d also expect copper to do the same. I think the answer to the oil vs copper bifurcation is perhaps due to the loss of Russian oil production being priced into crude markets. Copper prices are pulling back in the face of growth concerns alone since it’s missing such a positive catalyst.

Either way, I may have to call an audible and begin accumulating O&G service companies in the medium to long term portfolio.

Tuesday’s Trading Activity:

Wednesday 5/4/2022

After a lot of contemplation and discussion with some of my closest MinTwit advisors, I decided to call an audible early Wednesday in order to mitigate the chance I was positioned incorrectly on two important issues:

In case Powell were to say something dovish in the Fed day presser.

In case oil & gas does not pullback in the inflation unwind as I was anticipating.

I announced this audible and my thought process on Twitter in a short thread linked below:

I then began scooping up O&G service/drilling companies:

Once Powell subsequently made the off script dovish slip removing the 75 bps hike, I had to cover some of my downside exposure (UVXY, FNGD, and NVDA puts) and start buying O&G calls:

XOM

COP

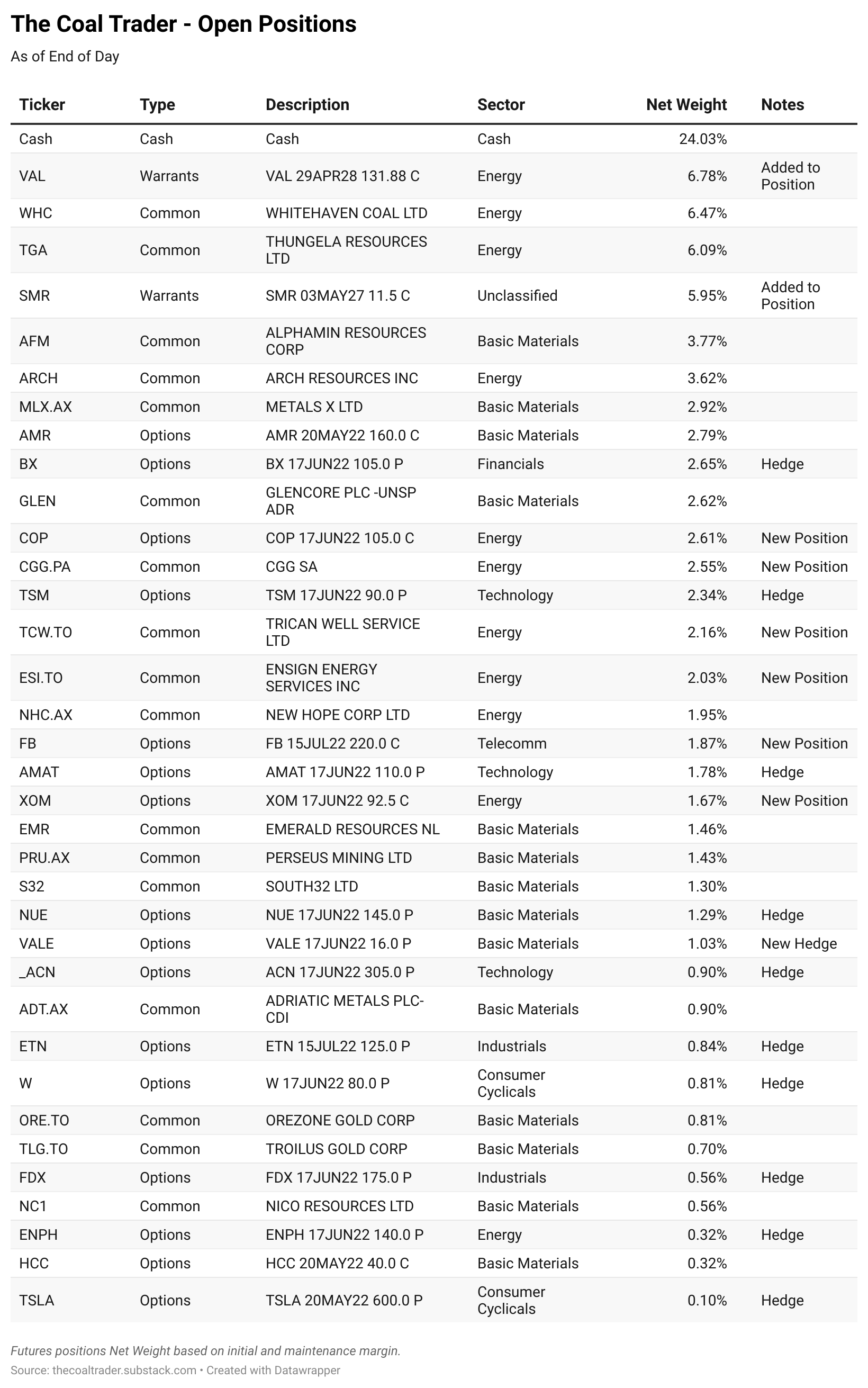

I also added to the VAL warrants position. Energy (which includes coal) is now 36% of my portfolio and Basic Materials is 22%. It was a rough day for the account due to all of the summertime puts on the books, but I’m not too worried. I feel comfortable with the pivot into O&G despite the lack of pullback, and I don’t think broad equity indexes are out of the woods at all.

Since I think Powell went off script, basically removing 75 bps hike on accident, my hunch is that his team of Fed-heads will soon be out in force with hawkish comments in order to take some of the recent euphoria out of the market.

Wednesday’s Trading Activity:

Thursday 5/5/2022

Broad equity index action on Thursday went a long way in confirming my general downside bias and summer selloff base case forecast. I think the rally post Fed presser lulled a lot of bulls and BTFD’ers into going long, only to be taken out to the woodshed on Thursday. Those bulls are now trapped and will soon turn into forced sellers, if they have not already. As I’ve said a few times before, the BTFD mentality is for bull markets only, and the bear market we’re in is about to provide a costly lesson to those not heeding this shift in mindset.

I did not trade it perfectly, perhaps not even very well however, when you realize you’ve made a mistake you have to move quickly to remedy it. On Thursday morning I set alert levels on the VIX, FNGD, and FB and told myself no matter what I would re-enter UVXY and FNGD, and close out the FB calls, once my alerts went off. One by one they were triggered and one by one I added downside exposure and removed long exposure.

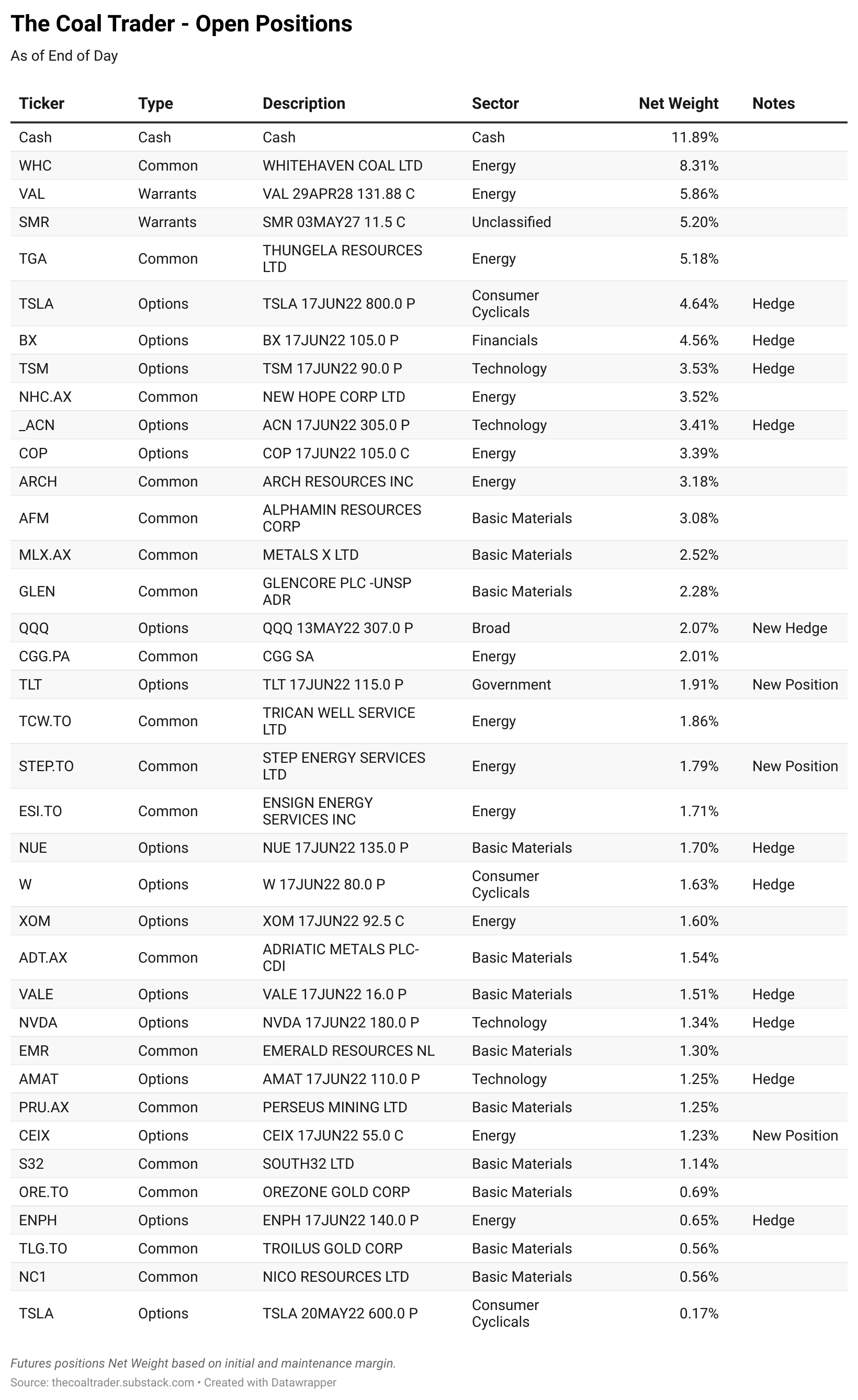

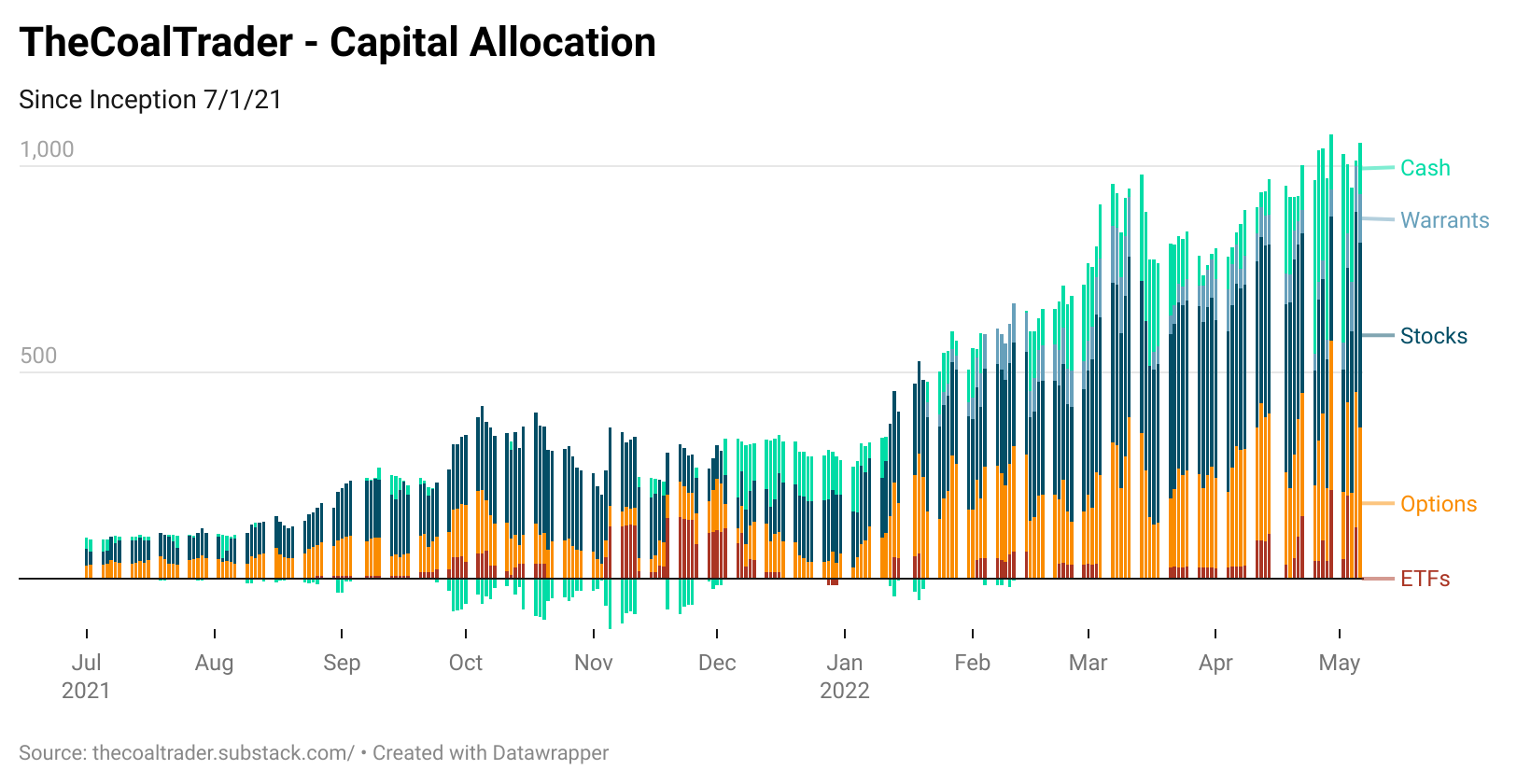

You can see my net cash position in the tables and images below. Since I entered into oil and gas longs on Wednesday to hedge the Fed Day pop, I basically ran out of capital to deploy short on Thursday. Oh well, I got whipsawed like almost everyone else.

AMR announced positive earnings, as anticipated, and ended the day up 3.4% in a nasty blood-red tape. This is a positive signal. HCC announced decent results but sales disappointed. The good news is HCC rebuilt a lot of inventories and those sales probably get pushed into Q2 where prices were higher anyway. I am not worried at all about their outlook.

Looking at pre-market S&P 500 futures as I write this and I think equity indexes will need to trade into the low 4000’s to clean up and retest some previous fills in that area, refer to the chart below:

Friday could get ugly depending on where buyers show up. Friday’s tend to be trend days that do not get reversed so the probabilities favor an ugly outcome. Good luck out there!

Thursday’s Trading Activity:

Friday 5/6/2022

Trading action on broad indexes Friday was mostly as I anticipated in Thursday’s pre-market commentary. The initial downdraft to cleanup unsettled business in the low 4000’s on the S&P 500 played out perfectly. The rest of the day was spent in that range cleaning up the fills and getting everyone used to the new range.

The “Charts of Truth” continue to point to lower prices and I’m going to maintain my overall bearish bias until that changes. Of course I’m referring to TLT and HYG here: as long as these two charts are making new YTD lows I think broad indexes will follow.

There’s one BIG exception - and that is ENERGY

You can summarize my entire strategy for the year as one simple pair trade:

Short QQQ - Long GNR (or pick your favorite natural resources ETF)

And although I got a little too cute for my own good expecting an energy pullback, going forward the following pair trade looks even better:

Short QQQ - Long XLE

Being long XLE gives you the perfect hedge for shorting tech. If/when the Fed finally pivots and broad markets put in a significant bottom, XLE will completely moon as well. Don’t overthink this.

Next week I’m going to write about the supply chain issues being caused by China’s no-covid policy and the negative ramifications on raw materials and manufacturing. I believe this is what’s causing a slump in metals and miners and I don’t think its going to last through the summer. There’s a very short term inventory cycle we’re living through, created by the initial covid lockdowns and once again being created by China’s current covid lockdowns. It’s compressing the overall business cycle and we’re likely to see a summer mini-recession followed by a mini-manufacturing boom which should lift metals and miners out of their slump. If this mini-inventory cycle corresponds with a Fed pivot, we’re in for quite the boom in the back half of the year.

Friday’s Trading Activity:

For those who want to follow my trades in real time, you can always upgrade to the Founding Member classification of this Substack to get access to TheCoalTrader private Twitter feed. Once you upgrade just send me a dm with your email address to confirm and request to follow the private account.

Monday 5/2/2022

Tuesday 5/3/2022

Wednesday 5/4/2022

Thursday 5/5/2022

Friday 5/6/2022

Please let me know if you have any questions with regards to strategy and positioning, or anything coal related.

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or it’s Content.

Where can I get the relevant live coal price for WHC, TGA, NHC please?

Why is the Domestic - Avg. Realized Price per Ton for Peabody so low ?

Is that because they have all kinds of long term contracts with domestic consumers?

And if so, any idea when (and how much) those contracts will be refreshed with more profitable prices?

They invested $40M in PRB and midwest and claim higher production. Any idea how much production that could be and will all that go against spot prices?

What on earth is this R3 Renewables agreement all about? Some woke virtue signaling or true insanity?