Initiating Coverage on Yancoal (ASX: YAL)

Strong buy despite M&A questions

An analysis of Yancoal should really be pretty simple. The company owns and reliably operates high-quality and low-cost, Tier-1 coal mining assets that are some of the best mines in the markets that they serve (mostly Chinese, and northeast Asian power plants). YAL is pretty much a pure play thermal coal producer tied to markets where coal will continue to be a solid player in the power mix for years to come. The company currently owns no extraneous assets that are problematic, a la Core Natural Resources (CNR) in the US, which is holding onto some low-margin Powder River Basin mines. Yancoal has no exposure to declining European coal burn. Just a nice, simple, solid business model. Followers of TCT will know that I like Yancoal because I’ve mentioned it during the AMA post that I did with Matt back in November and at other times.

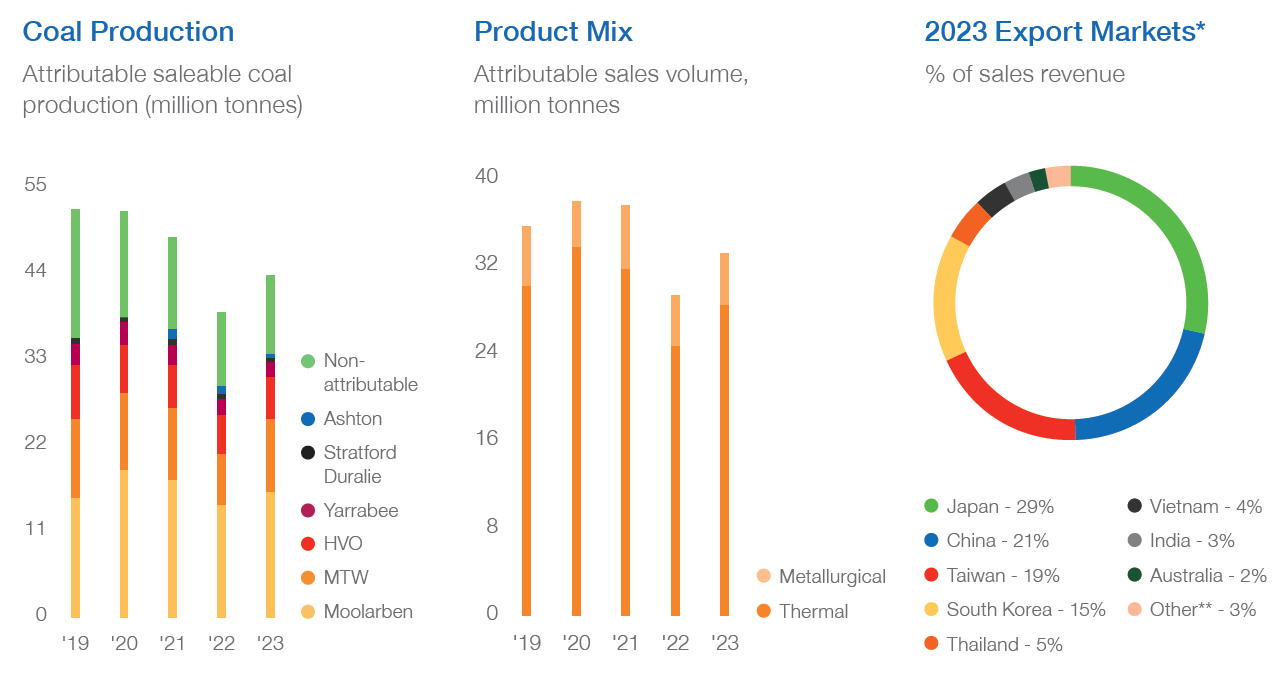

Source: Yancoal Fact Sheet 2024

Around 85% of YAL production is thermal coal and the remainder is met coal. About a third of the met coal produced has historically been sold as Pulverized Coal Injection (PCI) coal and the rest is a combination of semi-soft and Tier-2 hard coking coal (HCC).

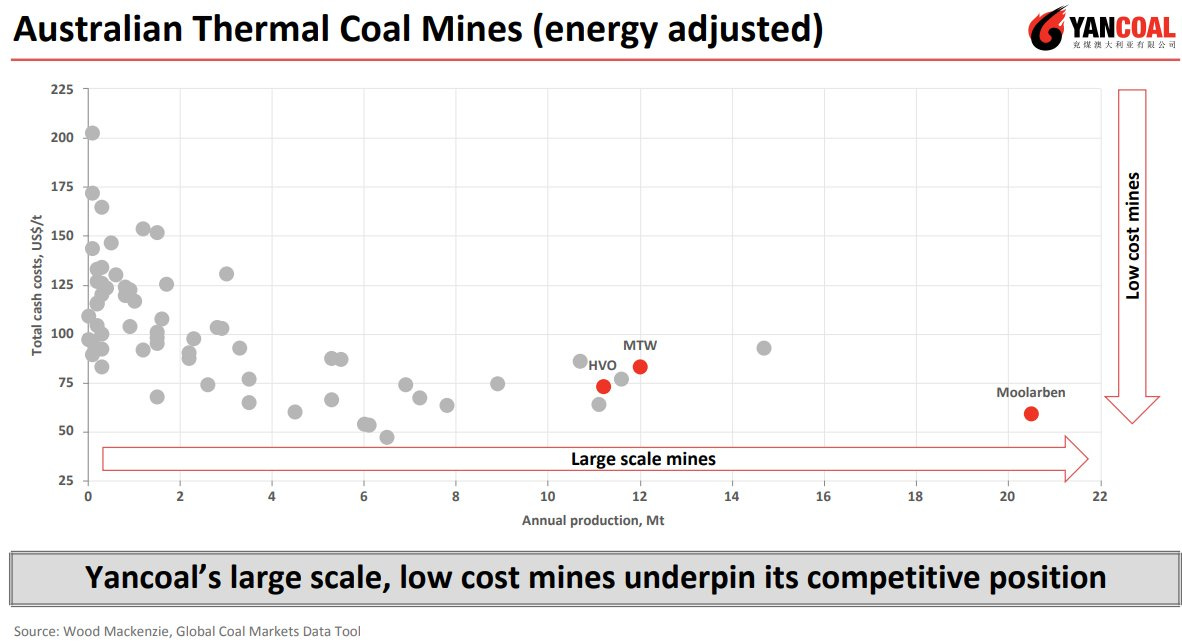

As shown in the image below, Yancoal has large-scale mines that can ride out almost any thermal coal price cycle. The majority of YAL’s output has cash costs below about US$80/mt (basis 6,000 NAR coal, fob Newcastle). FCF shouldn’t turn negative until Newcastle high-cv prices drop below US$75/mt, which is a remote possibility. YAL cash margins did turn slightly negative during the COVID-19 lows of 2020-21, but not for long.

Yancoal’s relative simplicity is why it’s such an easy stock to recommend to people. It’s straightforward, cheap, unlevered, and has plenty of FCF. In the last quarter of 2024, in a down market, the company added $A480 million to its balance sheet. As Yancoal currently trades with an Enterprise Value (EV) of under A$6 billion (including all the freshly minted cash from Q4 2024), that implies an EV/FCF ratio of just ~3x. The company is holding A$2.3 billion in Net Cash, which is nearly 30% of its Market Cap of ~A$8.4 billion. The FCF yield (TTM) is running at over 20%. I could cite additional, impressive statistics, but basically there is no better-capitalized company or superior value play in the coal equities space. So, I’ll tap into the infinite wisdom of coaltwitter for a pithy quote to sum up Yancoal: the ultimate “gentleman boomer yield stock.”

That has kept Yancoal shares trading above peers over the last year. The only stock more bulletproof has been ARLP, which I wrote about earlier this year.