Hallador Energy (HNRG)

Hallador Energy (HNRG)

Summary & Back of the Napkin Pro Forma

Hallador Energy, ticker symbol HNRG, owns Sunrise Coal which is a thermal coal producer currently located in the Illinois Basin (ILB) and predominately in the State of Indiana.

Oaktown Mines

The Oaktown complex has a stated productive capacity of 8 mtpa. Mining is done using room and pillar methods with continuous miner units. The tons are conveyed to the surface from each mine where they are washed before being loaded onto rail cars or trucks. The complex is connected to a rail loadout that can store two 120 car trains and is serviced by CSX Railroad and Indiana Railroad.

As stated in the 10-k, Sunrise sold 6 million tons of coal to 11 power plants in 5 different states across 9 different customers in 2020. However, 74% of 2020 sales were shipped within Indiana alone. There are no export sales.

Their thermal coal reserves have the following stated coal quality:

Btu/lb ranges from 11,200-11,600

Sulfur is high and ranges from 5 - 6.5 lbs of SO2/MMBtu

Chlorine is low, typically < 0.12%

For those looking for for some reference material on coal quality and coalification, you can start here.

The coal marketability is “ok” for the ILB, the chlorine is low but the sulfur is high. High sulfur in thermal coal is a problem due to higher costs during post combustion SOx elimination methods. You can read more about desulphurization here. Basically the power plants incur higher costs while scrubbing the SOx from the flue-gases. Most large power plants have implemented these technologies and emissions have been significantly reduced as a result. The EPA has a pretty cool page where you can visualize the emissions trends here. High chlorine in thermal coal can be problematic due to its corrosive properties which degrade the boiler materials and leads to higher maintenance costs. You can read more about chlorine in coal here.

Like all Indiana and central Illinois coals, the problem is not really about marketability of the coal from a quality standpoint, the problem is simply that they are at a competitive disadvantage from a logistics standpoint. They have no river access and so they’re basically isolated to primarily serve the local market .

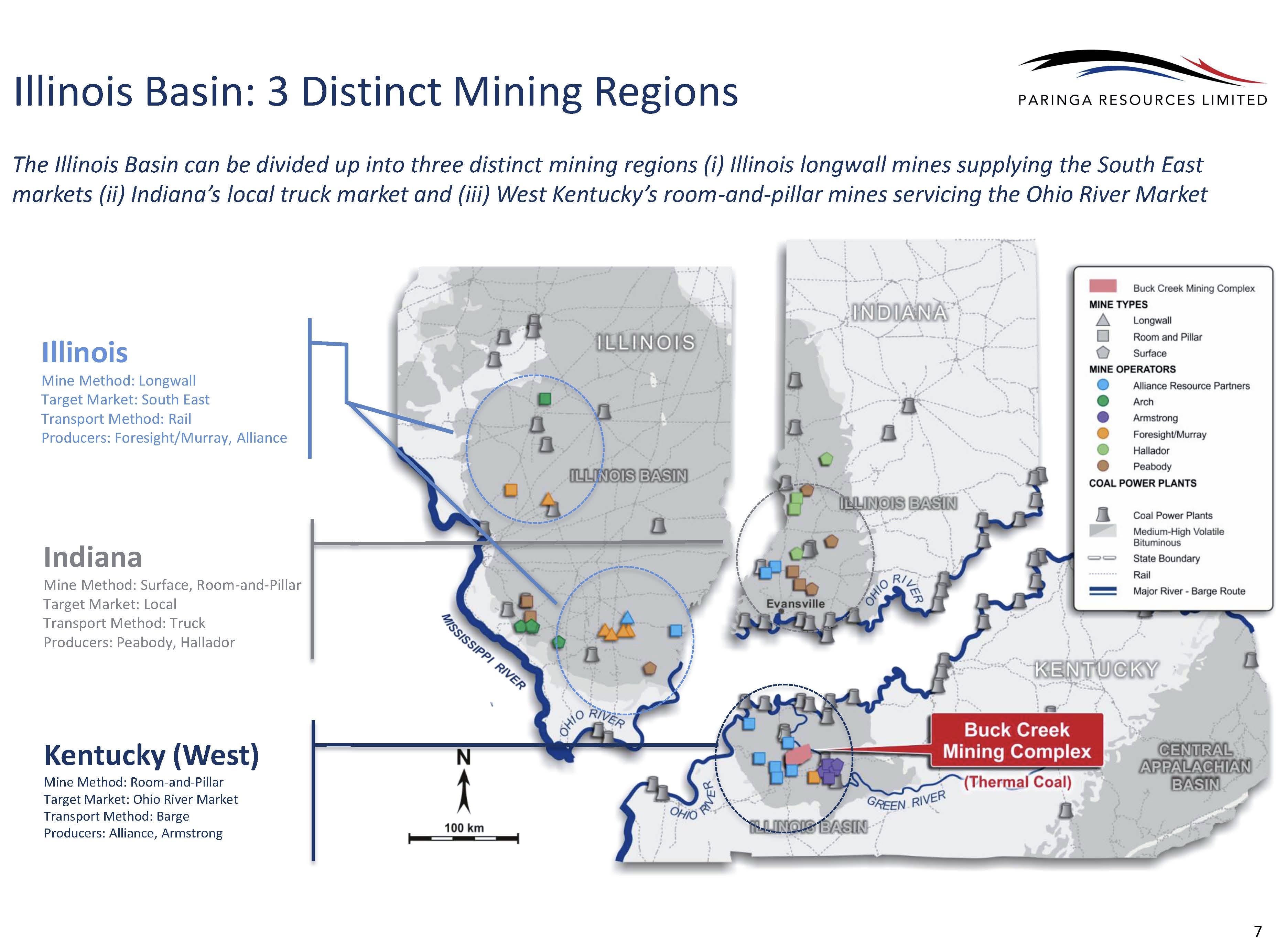

The following is from a Paringa Resources 2015 powerpoint, it’s old but it’s a good map to visualize the situation:

The two Oaktown mines are the green squares located on the western border of Indiana. You can also see the coal fired power plants (keep in mind some of these may have been retired since 2015) in order to get a visualization of the marketplace. So it looks like they’re serving the power plants in central Indiana and central Illinois, with perhaps a trickle going out to customers a bit further. In 2020, 79% of Sunrise’s revenue were from 6 power plants, and if you were to draw a circle around the Oaktown mines you can easily determine which ones those are.

Pricing Power

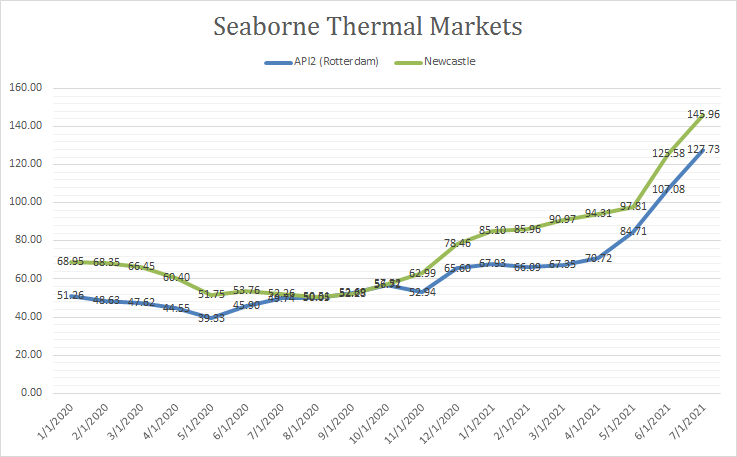

The bullish thesis on thermal coal hinges on structurally higher natural gas prices, and I have been pounding the table for over 3 years that it’s coming. Now that we’re living in a world with Henry Hub prices greater than $4/MMBtu, you should expect coal utilization to expand in US - and in a more permanent way. Moreover, in a world where European gas prices are at 16 year highs and Asian coal demand is at all time highs, it’s no surprise that seaborne thermal markets are rallying hard.

Domestic thermal coal is typically sold through long term fixed-price and fixed-volume supply contracts which often last for multiple years. Some of the contracts include a predetermined price escalation for each year and a few even allow for price re-openers whereby price is renegotiated within some predetermined range. The key point I’d like to make here is that in a fast moving market, these long term contracts do a poor job of keeping up with price. This is valuable when prices are moving down because you don’t feel the full impact immediately, but it also becomes a liability when prices are moving up.

Hallador likes to tout the efficacy in their long term contracts because they believe it demonstrates how risk averse the company is situated. They state this directly in their earnings call, and explain that the market should re-rate them towards a higher multiple like they’ve seen in the past due to the long term nature of their contract book. However, the long term nature of their contract book means it will take a while for meaningfully higher price realizations to hit the company’s bottom line.

On the other hand, export contracts are more frequent, shorter in duration (often less than a year), and many times more price sensitive. Export contracts allow producers to see meaningful upside and allow them the optionality of ramping up production in good times to meet demand. This excess volume allows their mines to run more efficiently (especially the longwalls), lower their avg cost per ton, and maximize profit margins.

A good mix of long term domestic contracts along with export optionality is the sweet spot in the coal industry; it allows producers to naturally hedge a significant portion of future production and also capture excess revenue when prices rise in seaborne markets.

If you’re in the business of selling anything, the goal is to maximize market share and to maximize profit margins. Hallador is in a constrained market facing the risk that any of those top 6 power plant customers get idled/retired, and has no export optionality.

Pricing power in the coal industry is all about the competitive advantages inherent in the assets. These are things like:

Coal Quality & Marketability

Low Cost Mines (Longwall vs. Room & Pillar)

Transportation Infrastructure & Optionality

Location & Proximity to Customers and Ports

Port Capacity

Keep these in mind when picking which coal producers you’re investing in. I should probably do an article detailing the specifics of the above list.

Strategy

Sunrise recently permanently closed the Carlisle Mine in Q4 2019. It appears they’ve taken the rearguard action of falling back to Oaktown and their lowest cost operation in order to make a last stand. This is not surprising, as the demand for thermal has fallen over the last 5 years many producers have pulled out of their mines which are higher on the cost curve. As less tons are needed it makes sense to only produce the cheapest tons. Now they’re entrenched, but they’re in a “safe” and consolidated situation with low cost production, less maintenance CAPEX spread across multiple operations, and sufficient long term contracts in place to keep them in business while paying down debt. However, this is not a company on the offensive; they are not taking market share; and they do not have pricing power, as we’ve discussed above.

One caveat I will add is that Sunrise could be a takeover target. I’d imagine it would have to be in a distressed situation, but a buyer could come in and shut down the Oaktown complex, then fulfill the long term supply contracts from their own mines. Something to keep in mind, but that point in the cycle has likely already passed.

Outlook

Sunrise Coal’s mining costs in Q1 2021 were $28.88/ton, down from $31.07 in 2020, and $30.69 in 2019. I’m giving them the benefit of doubt here and saying their FY2021 cash costs will be approx. $28.58/ton. Therefore, the Oaktown move is giving them an incremental $2.42/ton profit margin, for an estimated total of $10.70 per ton mined in 2021. I have Q2 2021 net income being positive, mainly due to the jump in sales; I’m assuming they shipped more and lowered their inventory which was substantial at the end of Q1. FY2021 net income is still projected down, but only by around $500,000 which is probably within my forecasting error.

The proforma is below:

I’m assuming they sell around 5.4 million tons in 2021 and 5.8 million tons in 2022. Sunrise should be able to increase price realizations year over year and I have 2022 prices averaging $39.75/ton vs. $39.28 in 2021. As you can see, net income and FCF is expected to be positive in both years. With a current stock price at $3/share and a forward enterprise value of $208 million, the 2022E FCF/EV yield comes out at 13%.

As I mentioned in the Ramaco Summary article I wrote last week, I will be using 2022E FCF/EV as the main valuation metric for coal producers at this early stage in the cycle. Coincidentally, Ramaco Resources 2022E FCF/EV yield was also 13%.

Summary

I think Hallador Energy is indeed less risky than the market has it priced. They are in an entrenched position with visibility looking out over the next few years with very few hurdles in their way. The main risk is probably regulatory action from the Biden administration which forces the hand(s) of one or more of their key customers. Beyond that HNRG is a relatively safe way to buy a bombed-out coal producer for an expected forward yield which implies a higher stock price looking into 2022.

If you’re looking to buy exposure to the thermal coal global price rally however, Hallador Energy does not give you much. As I mentioned before, if you’re in the business of selling anything, the goal is to maximize market share and to maximize profit margins. Hallador does not have the ability to move the needle much in either of those directions. They’re in an isolated market geographically, and they therefore have no pricing power. From a competitive advantage standpoint, Hallador has very little of it.

My goal is to try to cover one coal producer per week so that we can compare strengths and weaknesses from a competitive advantage standpoint, as well as from a FCF/EV standpoint in order to determine which of them are “cheap”. At the end of this exercise I think you will find that many of them trade at yields similar or better than Hallador. Moreover, I think we will find similarly valued companies with the added benefit of all the competitive advantages, pricing power and optionality which should exist in our ideal coal producer. If we find that an ideal coal producer doesn’t exist, we will subsequently create a basket portfolio which contains the ideal mix we’re after in order to maximize returns while minimizing risks. That’s the plan anyway.

I hope this article was of value, feel free to provide me with any feedback necessary to make future articles even better. If you have any questions for me, please leave a comment.