Crude Oil Switch to Contango?

Crude Oil Switch to Contango?

An asymmetrical risk/reward bet is brewing

The Problem

Crude oil has a big problem, supplies are tight and the industry has been hampered with continual under investment, which has been going on for years. It doesn’t help when the IEA calls on investors to stop funding new fossil fuel projects and pundits are ignorantly forecasting peak oil sometime this decade.

Now that WTI is above $80/bbl governments are getting worried that energy prices may slowdown the economic recovery. The Biden administration is even begging OPEC+ to increase supply; I guess the 2022 election isn’t looking so swell for the Democrats. OPEC+ not surprisingly told Biden and company to pound sand. The little known secret is that OPEC+ probably doesn’t have the spare capacity to materially increase production, even if they wanted to.

Then there’s “ESG risk”, the new metric for financial institutions to judge their portfolios by. As Kuppy has said, ESG means “Energy Stops Growing”, and the thesis is playing out beautifully. ESG is causing capital costs for E&P companies to increase and in a similar vein as coal producers, they’re even starting to worry about potentially being shut out of credit markets sometime in the future.

The Solution

As with every commodity and business cycle, prices are the solution. In a Twitter discussion on European gas last night, Alexander Stahel had a good quote:

When things become expensive, price is the only voice among the deaf.

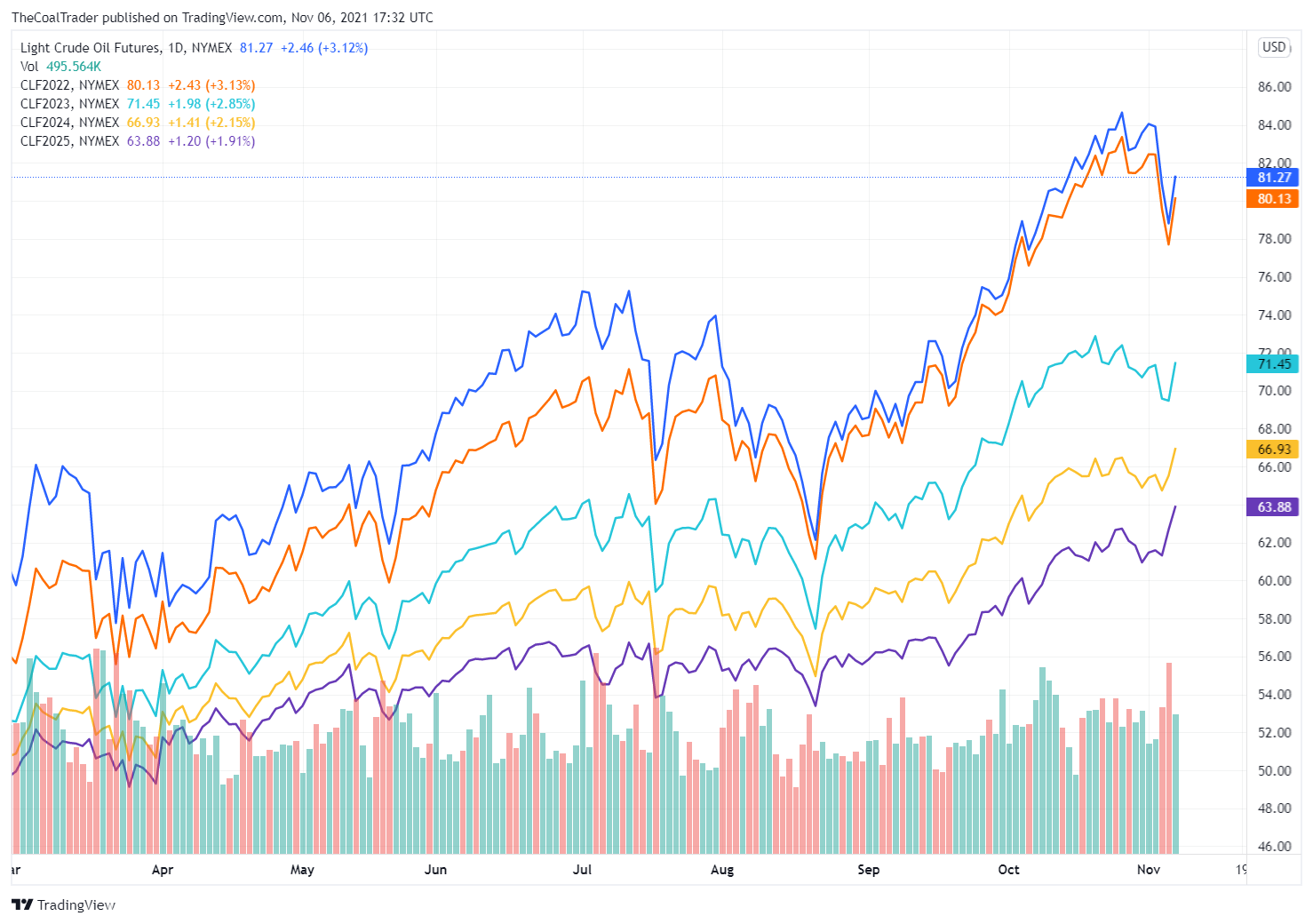

So let’s take a look at crude oil prices:

Crude futures are moderately backwardated. This means prices for future contracts are lower than current contracts. Think about the incentives inherently implied in this sort of term structure; the market is telling oil producers that prices will be lower in the future. This is not very stimulating situation if you ask me.

What would be stimulating in the perspective of an oil producer? What would incentivize them to go out and spend portions of their hard-earned FCF and invest in future production, against the will of the IEA, against the will of the ESG community, and against the will of shareholders who would rather see that money returned to their pockets via buybacks and dividends? The answer of course is much higher future prices.

The term structure needs to switch from backwardation to contango in order to incentivize oil producers to invest in future production.

If the term structure was in contango, oil producers could hedge and lock-in high prices which would de-risk capital projects.

Since this is the only solution other than economic collapse, this is what most likely will happen. If you look again at the chart above, there’s a very recent rapid move up in the Jan’24 and Jan’25 futures despite the recent dip in front month and Jan’22 prices. I think we’re witnessing the very beginning of the switch taking place, and the catalyst is OPEC+ refusing to increase supply. If OPEC+ can’t or won’t do it, higher future prices will have to stimulate the supply response.

The Trade

Unfortunately, the only way to trade this directly is via the futures market. I realize that a lot of the readers will not have the ability or the experience to trade futures, continue reading anyway as this may be instructive. I am admittedly a novice when it comes to futures trading, but the below setup is how I’m thinking about this potential setup.

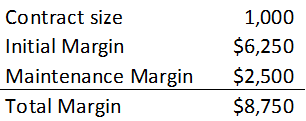

The trade setup is for 1 contract, and my IBKR margin requirements along with the contract sizes is below:

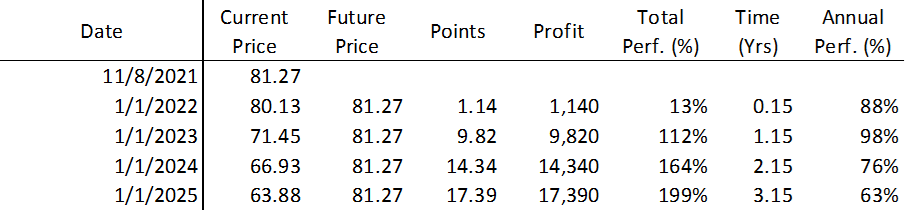

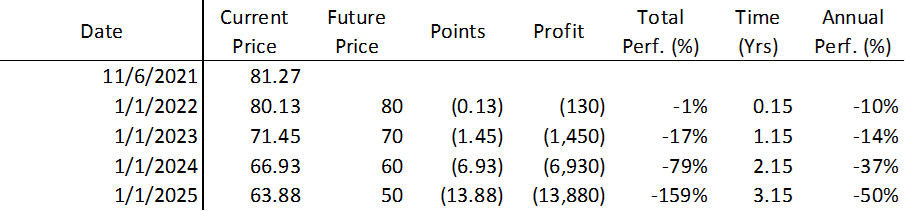

For conservatism, let’s say for now that I’m wrong and the term structure in the futures market stays exactly the same for the next 3 years, let’s call this Scenario 1. Therefore, in Scenario 1 front month WTI prices stay flat for the duration of the approximate 3 year period.

Scenario 1 is shown below and is basing the trade performance off of the total margin required to hold 1 contract for the duration of the trade:

Therefore, if front month WTI prices simply remain flat for the duration, owning any of the above contracts doubles the amount of capital you’d have to set aside in your portfolio for the trade (the total margin). On an annual basis the Jan’23 contracts would provide a return of 112% over the next 1.15 years until the delivery month, and the Jan’25 contracts would provide a 199% return over the next 3.15 years, an average of 63% per year.

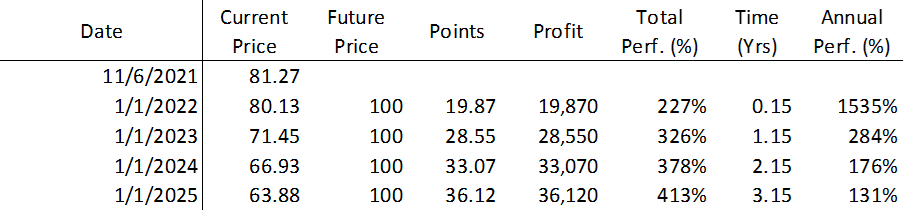

In the next scenario, let’s assume I’m correct and prices for each futures contract gets to $100 by the contract delivery month, review Scenario 2 below:

This is still a relatively conservative view. If we take the Jan’25 contracts, for example, this scenario is assuming front month prices rise 23% over the next 3 years. The outsized gain is due to prices for that contract itself moving up 57% from $63.88 to $100 during the period.

If the term structure were to flip from backwardation to contago, it would happen rapidly and the Jan’25 contracts would likely tag $100/bbl much sooner than 3 years. A rapid flip in the term structure would be the windfall scenario and I’ll let you guys model that one yourself!

The risk of course is that prices fall, and you can definitely lose more than your total margin. Let’s view a third scenario in which front month prices trend back to $50/bbl over the next 3 years. This demonstrates the inherent leverage of futures trading, refer to Scenario 3 below:

Summary

The risk vs reward asymmetry should be apparent in the three scenarios above. As I mentioned, I’m not a professional futures trader and there are most likely better methods to model potential scenarios than what I’ve shown above. However, the trade from a fundamental perspective makes a lot of sense to me and playing this setup utilizing crude oil with futures is a simple way to trade the situation directly.

There are other methods to take advantage of a crude oil shift towards contango. Other ideas would be offshore drilling companies, service companies, etc. which should all benefit from future capital spending in the oil space. Using futures eliminates all of the nuance and risk required in analyzing and betting on the companies’ management teams, equity and credit structures, valuations, etc. Moreover, utilizing futures earns a return off the very trigger which is necessary to incentivizes oil producers to step on the pedal and “drill baby drill” in the first place.

If you found this write up valuable please smash the like button below and if you have any questions please free to ask. I find all feedback helpful.

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or it’s Content.

Looking at what's available to plebs with no access to futures, I find USL which historically underperforms DBO. Until it doesn't (usually when the near months are in steep contango so DBO gets hammered during the roll). If your thesis is correct then it sounds like USL is getting ready to outperform again. But the option chain on DBO is so much nicer...

I'll be pondering this one for a while. 🤔

this is exactly my thinking! have been increasingly moving to futures to avoid business and political risk and just straight bet on CL. canadian government in particular could do anything, new minister is an intentional radical greenpeace guy. so even though i've enjoyed the stocks run and the value is still clear, the next stage might get harder (same feelings on coal btw)