Comparing Coal Equities

Comparing Coal Equities

Another Quick Visual Tour

There are a lot of coal producers to chose from, how do we chose which ones are worthy of deep research and perhaps our hard earned investment capital?

There’s two ways:

Fundamental Analysis

Technical Analysis

I’ve been covering coal producer fundamentals on this substack, but it’s a slow and hard process. I talk a lot about Competitive Advantages inherent in each producers assets, and how those advantages may or may not translate into pricing power.

On the other hand, technical analysis is an easy button.

Thermal Coal Producers

So let’s smash the easy button for now and compare thermal producer equity price performance:

This graphical viewpoint makes it pretty clear which thermal producers to buy IF you think the thermal fundamentals keep improving. At first glance you can see the performance ranking on the right hand side of the above chart. I purposefully chose this time frame to demonstrate a few things.

Although BTU is the clear leader in price performance, the volatility has been more extreme. The recent drawdown was much more severe compared to CEIX, WHC, NHC, or ARLP. Each investor/trader needs to consider their own risk tolerance and question whether they would’ve been whipsawed out of the position during the last drawdown. Maybe you want some of that upside potential in BTU but would prefer less volatility; there’s an optimal weighting mix somewhere with these names in order to make anyone comfortable with this trade.

Note that I removed Thungela Resources TGA (listed in London) from the chart above. TGA is a name I own and it’s simply killing it, leading them all:

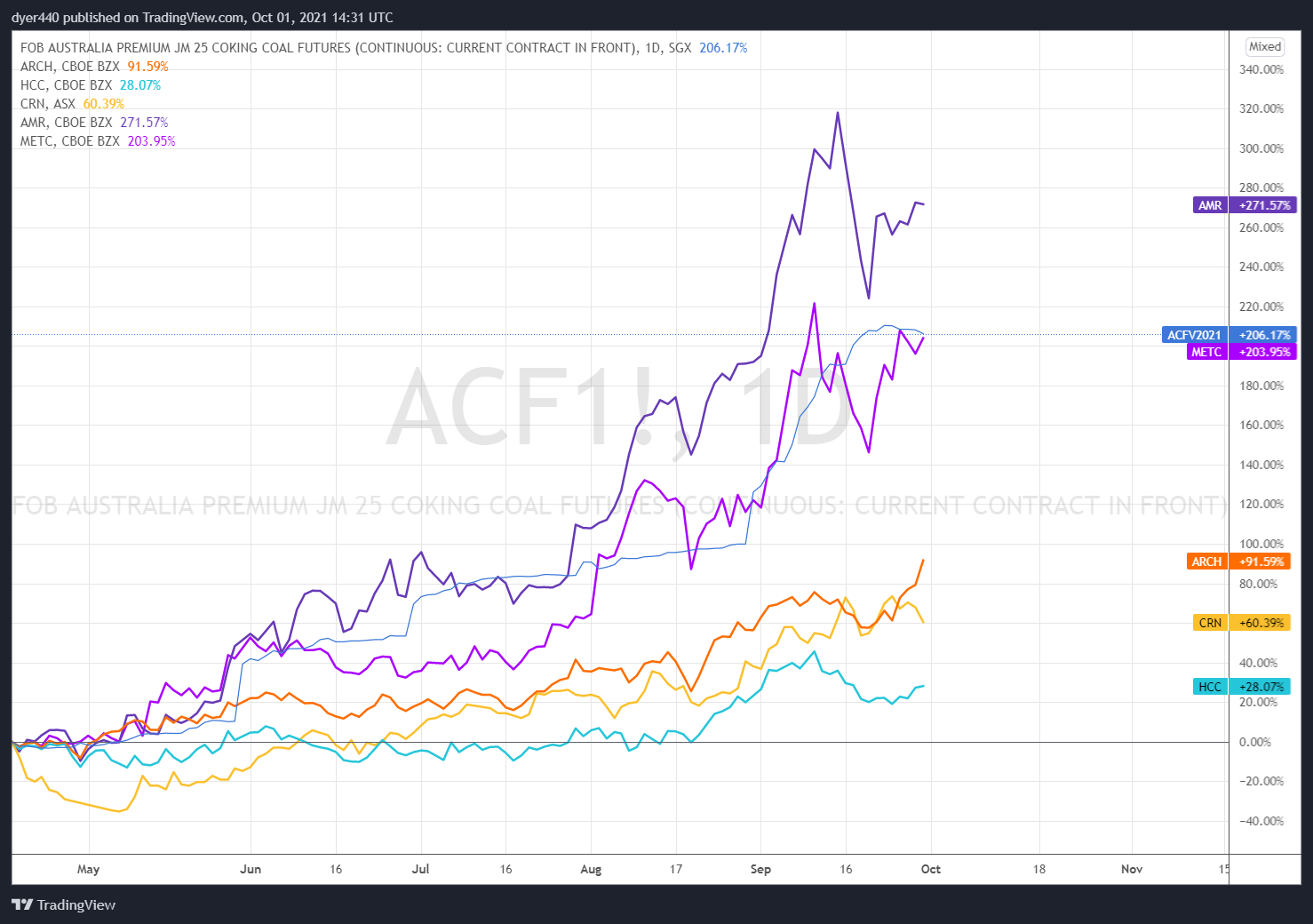

Metallurgical Producers

A similar story can be told if we compare met producer price performance:

The two price leaders are AMR and METC. From a fundamental perspective I would say that these two needed, or deserved, the biggest valuation re-rate from the start of this cycle. They were both very mispriced and basically left for dead. I’ll note that I think there’s some hype involved in METC’s rally since they’re an easy to move microcap, which is not even optionable at this stage. I owned METC early but I’m no longer involved (unfortunately!).

Now if we think in terms of volatility adjusted price performance, ARCH is killing it. You could’ve held on to ARCH easily since May and enjoyed a nice double. CRN got a late start to the rally and is attempting to catch up. HCC still has a strike in the way of it dominating all of these names, which it would be easily doing otherwise, in my view.

Conclusions

Everyone should understand the fundamental drivers of each investment they’re making. However, technical analysis allows you to quickly view the landscape of opportunities and determine which ones are worthy of a deep dive. I think this type of analysis works because when I view these comparative charts and rank each name according their volatility adjusted price performance, the names that should do best in terms of fundamentals, generally rank the highest.

Earnings season is just around the corner at the end of October. Earnings are a time where fundamentals matter and investor expectations come to fruition and materially move stock prices. The third quarter of this year witnessed the most extreme coal price rally I can remember, and I think producers with inherent competitive advantages and pricing power will have their day in the sun very soon.

If you think you would benefit from a deep dive into the fundamentals of these coal companies, please consider subscribing using the button below.

If you liked this article please smash the like and share buttons. Thanks for reading!

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person's use of or access to this Site or it’s Content.

Which of these is the biggest international exporter of thermal coal?