Coal Price & General Expectations

Term structure study of metallurgical and thermal coal prices along with my thoughts on the current rally

Intro

I did a Twitter thread on various commodities’ term structures without commentary, so I’ll add the commentary here. As much as I’d like to be a cheerleader for the coal sector I think we are in for a muddle through scenario for at least the first half of 2022. This is assuming a “normal” winter, which is probably prudent. Let’s discuss…

Thermal Coal

Let’s review Newcastle Prices and the forward 2022 term structure:

The chart above shows all the way back to the last cycle peak in 2017 and 2018. June’22 (in cyan) and Dec’22 (yellow) are currently trading in the same range of those historical highs. So front month Newcastle prices could fall 50% and still remain at/above those highs.

Let’s take a look at API2 (Rotterdam) coal prices:

Same story happening in Rotterdam. Current prices can get cut in half and they would still be above the last cycle’s high.

This should be incredibly bullish from a pricing standpoint for anyone thinking in terms of equity FCF on a full year 2022 basis. For companies like CEIX, TGA, WHC, NHC, and others, they should have an incredible year even if seaborne thermal prices get cut in half!

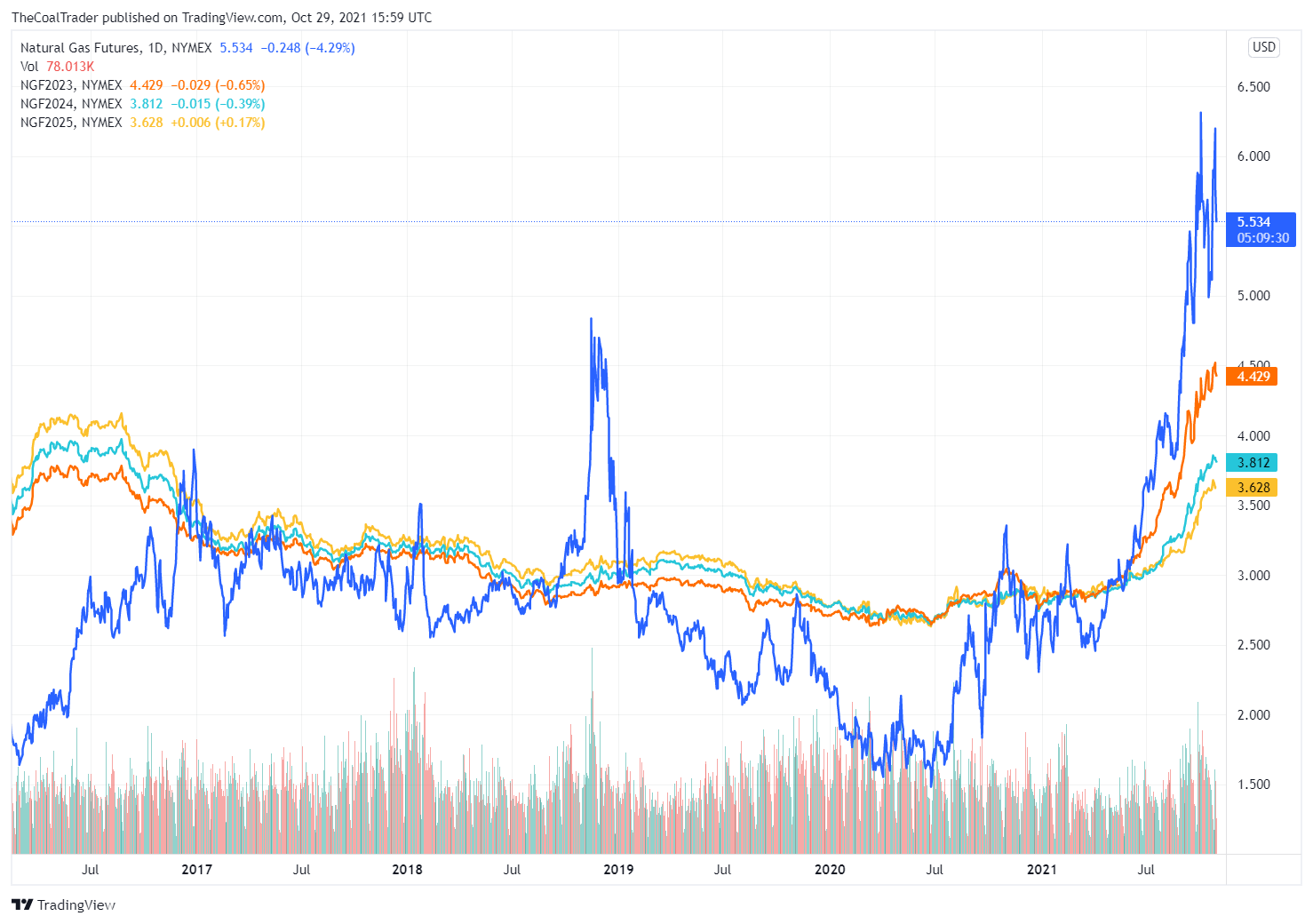

Natural Gas

US natural gas prices are very high, but more importantly the entire strip out for years is slowing starting to price-in structurally higher prices. Refer to the chart below:

Jan’23 prices are already priced at the same levels which spot prices rallied to during the 2018/19 winter of the ‘Bomb Cyclone’. That’s what I call a structural change. Although you can’t see it on the above chart, The ‘Polar Vortex’ winter of 2014 saw prices peak just under $6.50 per mmBtu, which is basically where we traded in early October of this year - during the shoulder season.

This backdrop of structurally higher natural gas prices should provide a fundamental tailwind for US domestic thermal coal producers like BTU, ARCH, ARLP, CEIX, and HRNG.

Met Coal

In similar fashion to seaborne thermal, metallurgical coal futures have blown through the highs from the last cycle in 2017 and 2018.

The first spike in 2017 was due to the Chinese limiting the number of days they’d allow coal production during the year (think about the 180 central planners have taken since those days!), and the second price spike was due to a cyclone hitting Queensland, shutting down half the worlds met production. You can see how long term futures always pointed to prices around $160 or so, and even during COVID and the spot lows in 2020, long term futures pointed to a price recovery of $140. The long term price this decade has always been around $150/mt.

Met prices a year from now are pointing to $180/mt, which is approximately $200 lower than today’s price. That would be quite a drop. As long as China maintains annual steel production near 2020/2021 levels there is almost no chance of prices falling that much, in my opinion, unless the Chinese lift the Australian ban and the Aussies step on the production pedal.

However, I can easily see prices falling back to the $250-300 range. How would this impact met producers? I think it would not be ideal, of course, but it would definitely NOT spoil the party for companies like ARCH, AMR, HCC, and METC.

Each one of the prominent met producers will turn into FCF monsters during 2022.

Summary

There’s one problem with all this bullishness. This is a sector where lobbyists have convinced politicians, who’ve convinced financial institutions to stay away. There’s really no hope of large passive institutional capital flowing into the space in a material way. The only respite will be buybacks and large dividends, but that can only take place once the debt is cleared off the balance sheets.

Coal producers have to pay down their debt. I think they will probably tread through 2022 very conservatively from a capital allocation standpoint. Executive teams are worried that the credit markets are going to shut them out from refinancing their long term obligations. I therefore anticipate huge debt repayments for the next few quarters. Investors will probably become very frustrated with this capital allocation strategy and the share prices will linger despite very cheap valuations.

In a normal market and a normal sector, value investors would flock towards companies earning quarterly FCF’s at 5-15% of market caps, and paying down huge chunks of debt. In a normal market in a normal sector all of these companies would be huge buys and analysts would be pounding the table in research reports, telling the world about this amazing valuation story. But this isn’t a normal market and a normal sector. There’s only like three analysts covering the industry and they’ve seen so many bankruptcies I doubt they even believe valuation story themselves.

So how’s it play out? I think these companies will generally do very well for the next six to nine months. They will be the FCF monsters everyone expects. However, spot coal prices will probably continue to correct lower which will be a drag on share prices. If companies come out and announce a clear and concise capital allocation strategy, which highlights buybacks and/or large dividends, then I would expect shares to rally. Otherwise, I think we’re in a place where shares muddle through, waiting for clean balance sheets to clear the way for buybacks.

About Met coal production expansion. If prices stay where they are, won't these companies be able to finance growth with retained earnings? Is institutional capital really needed? Maybe HCC has an additional hurdle of waiting for strike resolution clarity before resuming the Blue Creek project.