China's Australian Coal Ban

China's Australian Coal Ban

And the Impact on Metallurgical Coal Prices

Intro

I’m going to assume everyone reading this is caught up with the story behind the Chinese ban on Australian coal imports. If not you can read a good synopsis here.

This article is going to graphically show the impact from China’s ban on a few metallurgical coal indexes. I’m going to use the China CFR (data sourced by IHS, known as MCC4 China CFR low-vol PHCC), as the proxy for the price of met coal delivered to northern Chinese ports; you can read the methodology here. For met coal priced FOB Queensland, Australia, I’m going to use the Australian Premium Low Vol index (published by Platts, description here). For US met coals, priced FOB East Coast, USA, I’ll be using the US Low Vol HCC index (published by Platts, methodology here).

Price Reaction to the Ban

Below is a chart of the above listed met price series going back to January 2019. You can see the prices begin to diverge in early November 2020 when the Chinese ban was announced:

The ban signaled to the market that met coal supply was in for a period of disruption, especially for Chinese steel producers, and the CFR China price began to rally. Meanwhile, Australian PLV prices stalled as demand for met coal sourced from Queensland was thrown seemingly into a state of shock. US Low Vol was slow to respond but eventually began marching higher with China CFR as traders figured out the arbitrage opportunities and began pushing US coals into China in order to backfill the void left by the displaced Aussie coals.

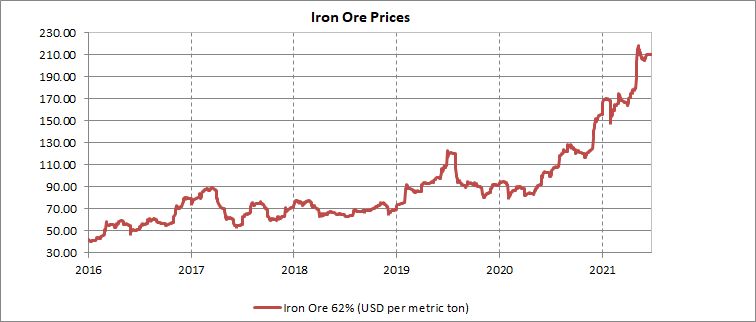

In a similar fashion as to what happened in 2016 when China made headlines which signaled the start of the previous up-cycle, I think the Aussie ban was a splash in the face to market participants, to wake them up to the fact that finished steel and iron ore prices were rallying while met coal was still enjoying nice long post-Covid nap. Refer to the charts of iron ore and finished steel below:

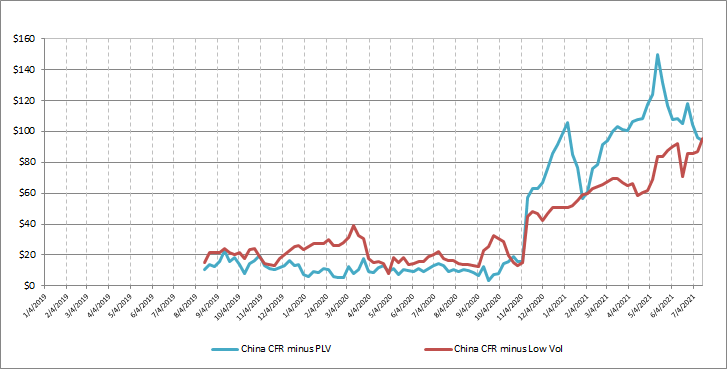

Now that met market participants are awake, they’ve been busy trying to work out the inefficiencies in the post-ban marketplace. I firmly believe that as time creeps forward, the process of buyers and sellers meeting at a fair market equilibrium will become more seamless and spreads, which have been blown out, will revert back towards historical norms. Refer below to the China CFR vs Australian PLV and China CFR vs US Low Vol spreads:

All else being equal, I expect these spreads to eventually compress back towards historical norms. There is some nuance of course with respect to the arbitrage taking place, such as shipping differentials or various quality differences inherent in the market, but in general I expect them to tighten.

If we take that assumption, and then also assume that demand remains constant into the end of year, what are the implications? The implications are for both Australia PLV and US Low Vol to both trade at approximately $290/mt. Today they are both priced around $214/mt which would imply a 35% rally into the end of year.

Spreads tightening basically means Aussie PLV and US Low-Vol chases the China CFR prices higher. We’ve seen this occur since mid-May as the Aussie PLV caught up to US Low Vol, which it is typically ahead of by $10-20/mt. US Low Vol is probably suffering a bit lately from it’s own success as shipping rates have also been increasing in response to the new trade flows, somewhat putting a lid on pricing:

What Happens if the Ban is Lifted?

To prognosticate on what would happen in the unlikely event of the ban being lifted, you have to ask yourself whether prices have been rallying this year due to the ban or due to demand. As I mentioned earlier, I believe prices have been rallying due to demand. You can see the signs of demand strength in iron ore prices and, more importantly, finished steel prices trading at all time highs. I therefore think if China lifted the Australian import ban, it would be a huge “nothingburger”. Trade flows would re-adapt, spreads would tighten anyway, and the China CFR price would continue to dictate the global price of met coal as it does today, regardless of the ban.

Opponents to this view can look at the China CFR chart and point to the fact the inflection point, the point when prices began rallying, coincided with the ban announcement. While I agree they coincided, I believe it was simply a wake up call to market participants and left sellers in a position of strength when negotiating with buyers. All it takes is China, the world’s largest consumer of met coal, to start making disruptive headlines to put the negotiating power back into the hands of coal producers, and as we’ve seen prices have been rallying ever since.

Please let me know if you found this article informative and/or you have any questions. I appreciate the feedback and would be happy to answer anything if I can.