API2 Prices in the Absence of Russian Coal

API2 Prices in the Absence of Russian Coal

US coals are unable to replace Russian coals in Europe

I’ve been thinking about the Russian coal ban which is set to go into effect on Aug. 10 in Europe. This mainly impacts the API2 thermal futures at the delivery point of Antwerp-Rotterdam-Amsterdam (ARA). So far we’ve seen a rapid buildup of thermal coal inventories at ARA ahead of the deadline, but once we move past Aug. 10, what is going to happen?

Some respectable analysts have mentioned they believe the price impact has already occurred and not to expect any more fireworks post Aug. 10. I completely disagree. Price is correlated to inventories and we saw prices initially spike on the news but then retreat as inventories were building. Once we move past Aug. 10 I think prices will have to spike higher again in order to pull volumes from other destinations into Europe.

When I think about the potential for US coals to replace Russian coals at ARA, I believe there’s a fly in this ointment, and it’s in the form of sulfur. US coals have higher sulfur content compared to the API2 futures specification, which is 1%.

Illinois Basin (ILB) is generally 3.0% sulfur (or higher)

Northern Appalachia (NAPP) is generally 2.5% sulfur

There is a sulfur penalty charged to US coals in order to blend down the sulfur content to meet the spec. You can think of the sulfur penalty as the cost to help offset the purchase of another coal which is below spec in order to blend the two coals together to meet the overall sulfur spec.

The sulfur penalty moves up and down daily depending on the amount of high sulfur coals being blended. At times when there’s a lot of ILB coal being shipped to Europe, for example, the sulfur penalty goes up implying the cost to blend all of the ILB coal down to spec is becoming an issue. When there’s no high sulfur coal being imported into Europe, the sulfur penalty goes to zero.

Here’s a chart showing the weekly sulfur penalty (grey, right hand side) compared to the API2 spot price (blue, left hand side), and the ocean freight cost from Mobile to Rotterdam. These are the inputs to calculate an estimated netback for an ILB producer. The netback is the price the producer earns on the sale:

You can see the gray dashed line went to zero during late 2019 and 2020. That’s because there was very little US coal being exported to Europe during that period. You can also see the spike on the news of the Russian ban earlier this year. That’s in anticipation of a lack of Russian coals to blend down the sulfur on US imports.

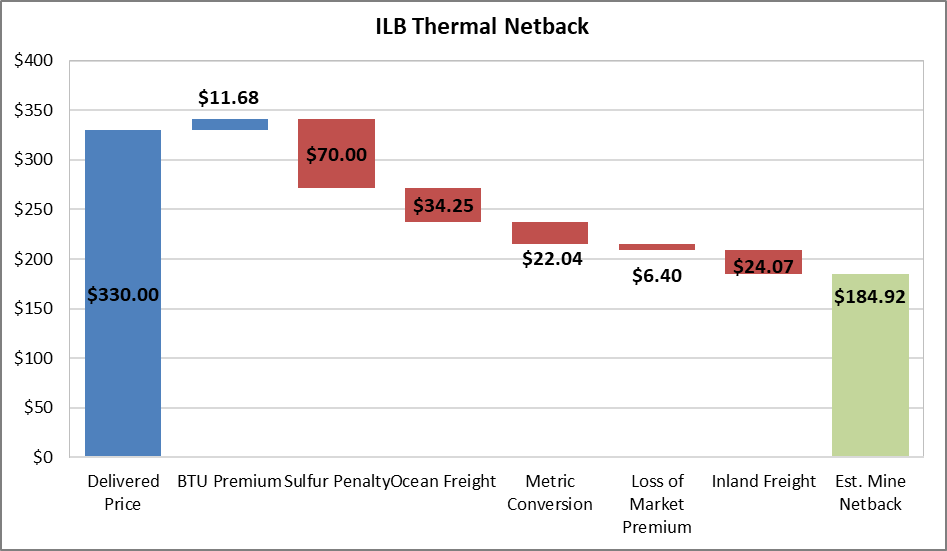

Below are two waterfall charts showing the current sulfur penalty at $3.50 per 0.1% sulfur, and the estimated impact on NAPP and ILB imports, compared to the $10 per 0.1% sulfur penalty which we saw at the peak:

At $3.50 per 0.1% sulfur:

At $10 per 0.1% sulfur:

You can see the stark difference. Even with NAPP coals which enjoy a BTU premium, there’s is almost a $100/mt difference with a high sulfur penalty. Moreover, the netbacks for ILB exports in such an environment make it almost not worth the trip.

So here’s the bottom line:

US thermal exports cannot replace Russian imports in Europe by themselves. API2 prices will need to go crazy-high to compensate for the US coal quality deficiencies.

What are the implications?

API2 spot prices will need to go high enough that they pull low sulfur coal into Europe. Given that everyone will be competing for the same coal, the world needs US exports. In the absence of Russian coals, I think the sulfur penalty is going to go crazy-high. API2 prices will therefore need to also go crazy-high, enough to compensate for the sulfur penalty, even for ILB imports. As we’ve seen in the example above, current prices at $330/mt would not be high enough.

ILB and NAPP producers will not enjoy as much premium in the marketplace due to the sulfur penalties. In the absence of Russian coals, the sulfur penalty could very well go above the $10 per 0.1% mark, and it will negatively impact US netbacks alone.

Other producers in the Atlantic basin will benefit to the US producers detriment. Specifically, high calorific value (CV) coals from Colombia (Glencore) and S. Africa (TGA).

I think the lack of Russian imports in Europe will go as far as pulling Newcastle coal out of the Indian and Asian markets into Europe as well. This will lift Newcastle prices. Basically every producer on the planet with export access and low sulfur coal will broadly benefit.

Please let me know if you have any questions or comments!

And if you’re not already, please consider signing up for my daily commentary and trading/investing activity:

Nothing in this Site constitutes professional and/or financial advice, nor does any information on this Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. The author of this Site is not a fiduciary by virtue of any person’s use or access to this Site or it’s Content.

I have been aggressively accumulating arch shares with the notion that this company may be best of breed in the domestic coal sector. Arch has a 50% FCF distribution policy implanted for now and the future. When I do the calc on this and it’s future outlook the annual return on investment appears to be ~38%. I am missing something?

fantastic note. thank you!